The Ironic Word of the Year

The Ironic Word of the Year

Central bank epiphanies, 2022 capex boom, macro week, earnings wrap, tech deflation

Central Banker Epiphanies

Our candidate for the ironic word of the year in 2021 is “transitory,” just as “unprecedented” was in 2020. This week, several central bankers who had responded to the pandemic using their global financial crisis playbook scrapped the transitory narrative. The Bank of Canada kicked off the front-end fun when they ended QE cold turkey on Wednesday. Later that afternoon, the Brazilian Central Bank raised their policy rate 150bp and guided to another 150bp in December. That night, the Reserve Bank of Australia ended front end yield curve control that was capping rates at 10bp out to April 2024, and 2-year notes jumped from 20bp to 78bp by the end of the week.

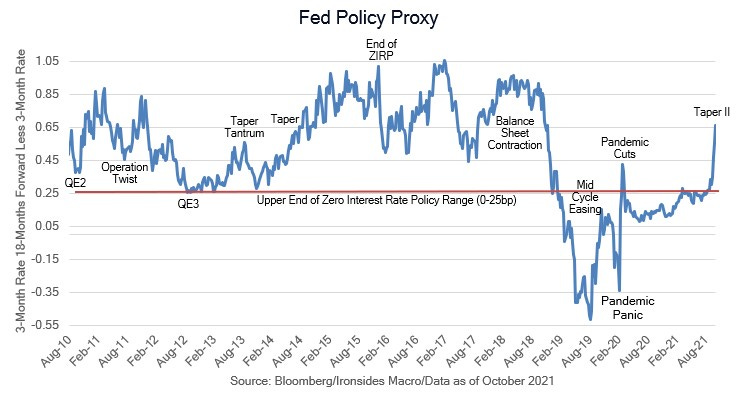

Meanwhile, as the November FOMC meeting at which the Fed is set to begin the reduction of large-scale asset purchases approaches, our Fed policy proxy continued its ascent as market participants priced additional rate hikes, as well as a shorter, sharper business cycle, with a lower terminal Fed policy rate. Where we think market participants are wrong about the longer-run outlook is the thesis, embedded in real and nominal rate curve flattening, that the terminal policy rate is even lower than last cycle’s 2.5% peak. More likely, the neutral rate (r*) is higher due to a number of factors, including the terming out of nonfinancial corporate sector debt that remains at a historically low level relative to GDP, additional household sector deleveraging and the lowest on record financial obligations ratio, stronger demand for capital, and faster productivity growth. Tactically, we suggest fading yield curve flattening and any related weakness in financials should be bought.