The Ghost of Dean Bullard

The Ghost of Dean Bullard

Waller's World, Not as High for Not as Long, Trouble with the Yield Curve

The Ghost of Dean Bullard

Much of the post-FOMC speculation has settled on what occurred to Chair Powell and the rest of the Committee during the quiet period when the Chair closed the discussion by saying it was premature to discuss rate cuts, to significant reductions in the Committee’s forecasts for nominal and real policy rates. Our leading thesis is that Governor Waller was visited in a dream by Dean Bullard the night before Nick Timiraos (Wall Street Journal) asked him about disinflationary rate cuts and Waller offered the only hint that the FOMC was about to begin the pivot process. In our overly vivid imagination, we suspect Dean Bullard told Waller he was wrong to have been so hawkish. He regretted his insistence on pushing the policy rate to 5% and his 6% ‘DOT’ was haunting him. He was concerned his business school students were going to work as baristas in the Starbucks union due to Wall Street and consulting layoffs. Political polls implied the engineering students were going to have to give up on their dreams of a green world and work in oil & gas. Dean Bullard told Waller he was right about the vertical Beveridge Curve; the Fed could bring down inflation without additional labor slack. The dream ended with Dean Waller showing Governor Waller his fate if he didn’t change his ways; teaching DEI to college students, chaperoning safe spaces, and having his lectures monitored by the progressive police. The FOMC meeting began with an impassioned Waller convincing the Committee that the Phillips Curve was turning them into a bunch of Scrooges. We are of course kidding, but it was fun writing this.

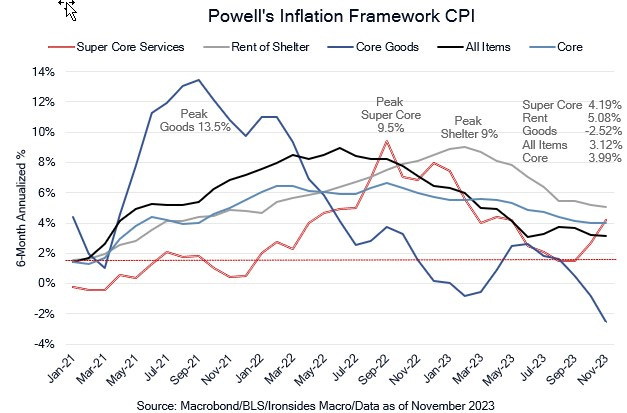

Either the Ghost of Dean Bullard visited Governor Waller, or Waller and the staff convinced the committee the evil twin curves (Phillips and Beveridge) going vertical was not an aberration, consequently, a continuation of core disinflation did not require higher unemployment. It could be the Committee thinks they know more about growth than market participants, the Commerce Department, or the Bureau of Economic Analysis due to a preponderance of qualitative data like the Beige Book and the intelligence gathering from regional bank presidents. Our work points to a decidedly weaker labor market than last month’s curious increase in the household survey implied. Another possibility was the third period of Treasury market instability during the tightening cycle brought them face to face with a sovereign debt crisis. In ‘24 the Treasury will refinance $7 trillion of the $27 trillion held by the public and needs to sell an additional $2 trillion in 2024 (estimates courtesy of former Dallas Fed President Kaplan on CNBC last Thursday). Consequently, we have the Ghost of Dean Bullard thesis, lower inflation forecasts, the Fed knows something about the labor market the BLS doesn’t, or sovereign debt crisis risk as our possible explanations of why the Committee abandoned the Phillips Curve framework, ended the hiking cycle and pivoted to a bias to ease we would characterize as ‘not as high, for not as long’. The earlier than expected pivot is important for investors but does not completely resolve the tight bank credit channel.