The Battle over the Budget

As trade policy pessimism fades, the focus shifts to Congress and the Reconciliation Bill, and the sausage making process is particularly messy.

Here is a video from The Schwab Network, Friday May 9th

The Budget Trumps Trade

The S&P 500 has retraced 61.8% of the February to April 22% peak policy pessimism correction as the Administration edges towards a more restrictive, but surmountable increase in global tariffs. This leaves the index 7.5% below the Inauguration Day level, about where we expected as growth slowed during the detox from government spending to a 2H25 recovery in private sector capital investment. We have long maintained the most important Trump Administration policy issue is stabilizing the growth of government debt, and in our view the only viable path is to return government spending to 20.5% of GDP, the 50-year median, by the end of the presidency. The news coming out of the House was disappointing this week, but until we see the House version of the reconciliation bill, we will withhold judgement on the debt and deficit outlook. The second most important agenda item is the restoration of corporate investment tax incentives; this part of the agenda appears on track, notwithstanding some economic illiberal individual and small business tax rate proposals.

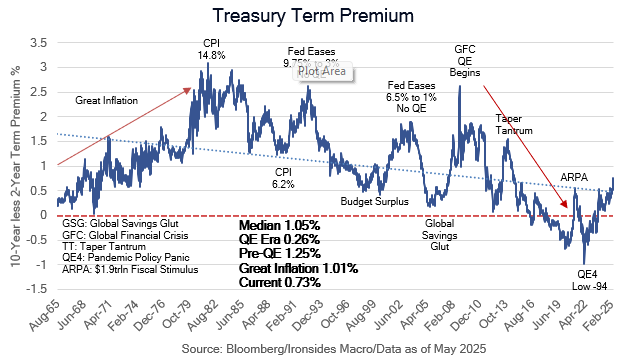

We expect the market’s focus to switch from trade to taxes and spending, in our view, the budget deficit is more important than the trade deficit for the outlook for capital spending, productivity, margins, earnings, income and output. Therefore, it stands to reason, the budget trumps trade for our outlook for equity and Treasury prices. Watch the Treasury market closely, if Congress waivers on their spending cut pledges term premium is likely to widen further, for the wrong reason.

In this week’s note we review the FOMC meeting with an interesting finding, the Fed put is an exotic option on the unemployment rate (we know that sounds complex, so read on). We preview the CPI report, dig in on tax and spending policy and examine the market implications with some sector ideas at the end of the note.