The End of Rate Suppression

Credit spreads imply low recession risk, extreme sentiment, 2023 rate cuts less likely, a structurally lower equity risk premium

2022 Year to Date, A Narrative Account

When we went to our university bookstore to purchase Paul Samuelson’s textbook for macroeconomics 101 and first heard his quip, ‘the stock market has predicted 9 of the last 5 recessions’, Fed Chair Volcker was kicking off the first of five recessions (so far) of our adult life. Over the next 4 decades there have been four more recessions and four false alarm stock market declines of 20 per cent or greater. Back in our Lehman days there was a legendary credit strategist whose work showed that credit markets were a more effective recession indicator, while stocks did a better job predicting economic recoveries. In our 2022 outlook note we expected a difficult first half almost exclusively attributable to policy tightening as the markets and economic activity diverged, that would be followed by a recovery of the losses in the second half — in other words a fifth false alarm. The ensuing correction pushed just beyond the largest of the recent Fed policy related corrections (2011 and 2018 20% drops) to the median recession related decline in the S&P 500 of 24%. This raised investor concerns of another recession, despite a lack of economic imbalances that are a necessary condition for a persistent and widespread contraction in economic activity.

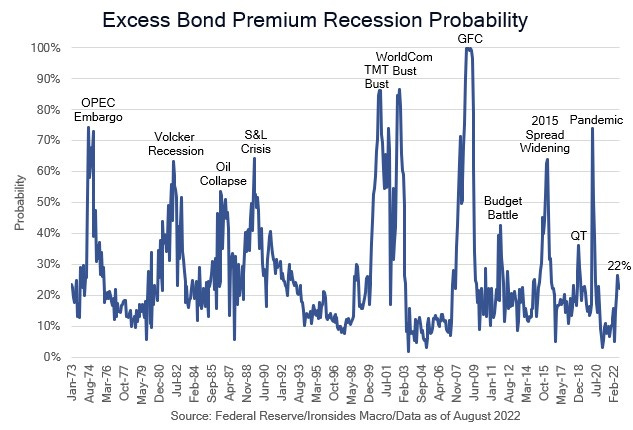

In June we reached the second of two crucial turning points, peak monetary policy tightening expectations leading to a furious rebound in stocks. The first was peak inflation, which also peaked in June though the market measures topped out in April. Three weeks ago, we concluded that of the three channels of QE/QT — liquidity, the portfolio balance effect and the level of longer maturity real rates (TIPS yields) — real rates did not adequately reflect the shrinking of the Fed’s balance sheet, leaving the markets vulnerable to a portfolio balance channel (taper tantrum) aftershock. That is precisely what occurred, as 10-year real rates spiked 50bp, the S&P 500 followed Joe Fibonacci’s (not his real name) blueprint, retracing 61.8% of the summer rally, and exchange rates of large energy exporters (euro, pound, yen and yuan) plunged. While the mother of all taper tantrums (Fed tightening risk-off) aftershock rocked markets, credit spreads lagged other risk assets as evidenced by the excess bond premium recession model that improved from a 26% probability in June to 22% in August. In short, the evidence that this is a fifth false alarm, not a sixth recession, is compelling in our view. Consequently, we are on track for our original 2022 forecast for a full recovery of the 1H losses, however the tail risk of an ‘87 Crash, the true mother of all taper tantrums, remains elevated and downside S&P puts are cheap. Given our expected upside for stocks, spending some capital on hedges you expect to expire worthless is rational due to the possibility (which we discuss at length below, as well as in last week’s note) that Fed tightening triggers a currency crisis.