The End of Cyclical and Secular Disinflation

The Path from 9 to 4, the secular outlook for goods, housing, energy and inflation as a fiscal limit

Apologies for the delay this week, our trip to NYC and Boston pushed the release back.

The End of Disinflation

In our 2023 Outlook note, ‘The Path from 9 to 4’, we forecasted favorable macroeconomic conditions and an abundant liquidity environment for stocks and bonds through 1H23. The path from 9% to 4% inflation was clear as we lapped the ‘Putin Price Hike’, a process that will be evident next week with an expected 0.2% monthly increase in May all items CPI reducing the annualized rate from 4.9% to 4.1% due to lapping a 0.9% increase in May ‘22. Next month will likely complete the disinflation process when we lap the June ’22 1.2% monthly increase that was primarily attributable to food and energy price spikes due to the Russian Invasion of Ukraine, pushing the annualized rate down to 3.26% assuming a 0.3% June increase.

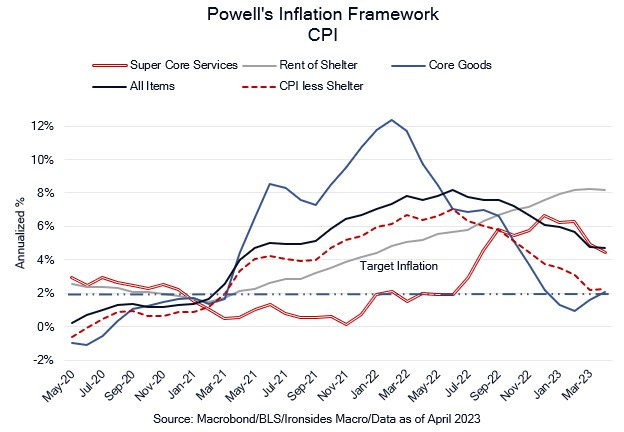

Through the second half we expect inflation to meander around 3.5% due to offsetting factors. Goods price inflation, the first order effect of the pandemic, peaked in February ‘22, bottomed a year later and has been moving up, though another leg down due to manufacturing producer price deflation in China and the auto sector coming into balance is possible. Food and energy inflation peaked a year ago, core services less rent of shelter peaked in September ‘22 and lag impaired rent of shelter peaked in March ‘23. We will not have a true handle on the underlying secular trends until early ‘24 when we will have lapped the direct pandemic effects, the policy response driven inflation, and the Russian invasion impact on food & energy. Our expectation is that there will be little doubt that the disinflationary regime of the ‘00s and ‘10s will be over as the underlying trend becomes clear in ‘24.

While Chairman Powell’s inflation framework, detailed in his November 30th Brookings Institute speech, does not include food and energy, the political pressure emanating from those important factors in the public’s inflation expectations should not be underestimated. Consider the President’s, or the Fed Chairman’s, approval ratings, and while the Fed professes independence from the political process, they hiked 75bp at four consecutive meetings while inflation was falling sharply from its mid-’22 peak. In other words, though core inflation will lag headline, leading to new-Keynesian thought leader calls for additional rate hikes, the drop in all items CPI will allow the Fed optionality, thereby allowing the June ‘skip’ to morph into a July pause, following the release of the June CPI report in a month’s time. The pause will be possible due to lapping the peak in core services less rents in 3Q22 followed by rents cooling due to the lags that prolonged the peak in shelter measures to March ’23 despite more timely measures easing 12-18 months earlier. While inflation falling from 9% to ~3.5% leaves policymakers, the economy and markets in a much stronger and more stable position, it is time for the Fed to Moonwalk (backup while appearing to move forward) away from the ill-advised 2% inflation target (more on this shortly).