The Corona Contraction Productivity Shock

The adversity/hysteresis effect, creative destruction and the costs of borrowing

The response to the last two notes we made available to all subscribers was incredible and these are exceptional times. Consequently, we are going to place this note outside the paywall for an additional week. We hope you will consider becoming a paid subscriber. Next week we will return to our format of a summary for free subscribers and full note for our clients.

The Next Stage: Solvency Concerns

We have moved to a new stage in the Corona Crisis, policy halted the run on the financial markets, resolving capital markets liquidity concerns. As we outlined last week¹, our business cycle and valuation analysis is consistent with the low on March 23 fully discounting the most probable fundamental economic outcome resulting from government population-based pandemic controls. One strong signal we have moved beyond the capital markets liquidity crisis, was the VIX falling nearly 20% and the VIX futures curve disinverting 10%, during a week when the S&P fell 3.9%. Another indication the March low fully discounted the Corona Contraction, was this week’s purchasing manager surveys and unprecedented labor market data failed to significantly weaken markets.

As we will explain, even in these early days of the Corona Contraction, evidence of the relative dynamism of the US economy is emerging, offering encouraging signs for the velocity of the recovery. What concerns us in this next stage, is that the crisis has exposed poorly constructed post-financial crisis policies, and the capital misallocation or malinvestment resulting from interventionist monetary policy is at risk due to the aggregate demand shock. We remain generally constructive on US equities, however, as we responded during our CNBC interview this week when the interviewer’s litmus test for a recovery was a strong recovery in air travel, economic contractions, with the exception of financial cycle collapses, have symmetrical recoveries, but not all sectors do. In other words, it is time to think about what sectors will come out strong when the population-based controls are removed.

¹https://ironsidesmacro.substack.com/p/gaining-traction-its-never-different

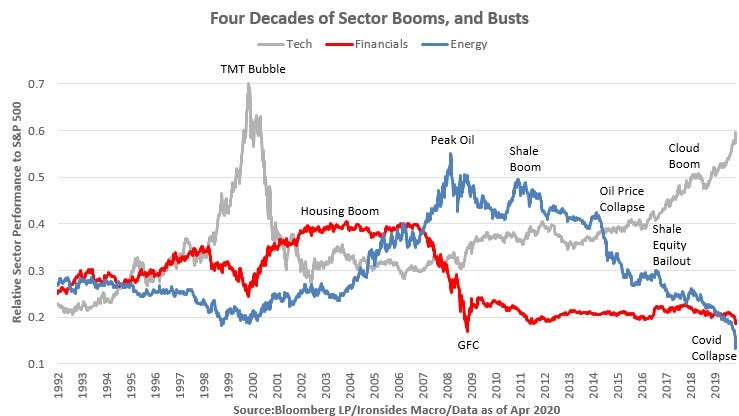

Figure 1: There were three investment booms and busts in recent decades, all three caused earnings recessions. In each case, the economy recovered but excess capacity for the sector at the core of the contraction lingered through the following business cycle. In other words, there might be a ‘V’ bottom for the economy, but not for the all sectors.

Creative Destruction

We once met with a contingent from the Austrian Central Bank and began the conversation by discussing Austrian economists Hayek, Mises and Schumpeter. They responded the only one they liked was Schumpeter. We found that curious since he reportedly died believing his prophecy that innovation would migrate from entrepreneurs to elite technocrats had been discredited. We suspect most policymakers responsible for post-financial crisis remain convinced that Schumpeter was correct, and if only pesky classic liberals like Paul Ryan had not obstructed them, their optimal policies would be working. Consider the mortgage market; policymaker’s insistence that the public have unfettered access to 30-year fixed rate fully prepayable mortgages creates a non-linear risk that cannot be absorbed by the private sector. When Bank America made the disastrous Country Wide Financial acquisition, they were left with a $1.5 trillion mortgage-servicing book that was unhedgeable. Fast forward to 2020, the capital charge on those assets is 250% and large banks are largely absent from the market. Meanwhile Federal Reserve purchases of agency mortgage backed securities effectively nationalized mortgage prepayment risk, causing more stable cash flows for servicers than would have been the case had this market been privatized. It seems in regulators haste to reduce risk to taxpayers by diverting these assets out of banks funded by federally insured deposits, the risk was not eliminated; it shifted to less regulated and well-capitalized nonbanks. The final step were policies that allowed deferral of mortgage payments. Thus far, policymakers are resisting the pleas from residential and commercial mortgage servicers. Policymakers seem to be willing to allow creative destruction forces destroy an industry their policies inadvertently created.

In the coming weeks, post-financial crisis policies that misallocated capital will come increasingly into focus. The Fed’s secondary-market corporate credit facility managed by BlackRock is unlikely to help the high yield, leveraged loan, collateralized loan obligations (CLOs), commercial mortgage-backed securities (CMBS) market, or real estate investment trusts (REITs), all of which benefited from the portfolio balance channel of quantitative easing, that created an insatiable reach-for-yield. While the run on capital markets is over, the broad drop in aggregate demand has impaired the cash flows of many of the assets underlying these securities, and in some cases like commercial real estate, the impairment might be extensive enough that the liquidity concerns evolve into a solvency crisis. Credit for private equity and venture capital investments are additional of areas of concern.

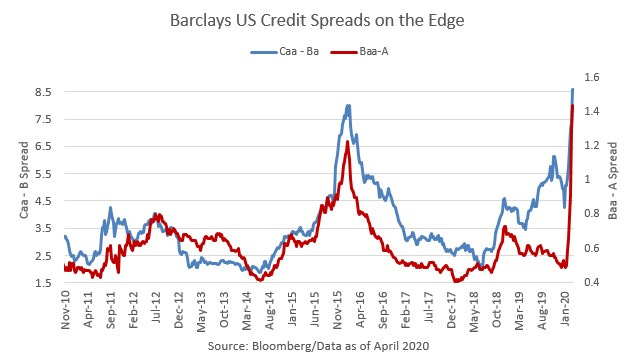

Figure 2: The lowest rated investment grade and high yield sectors are wider relative to the next credit tier than was the case during the oil collapse. We have not reached 2008/09 peaks of 230 bp and 11% for the IG & HY spreads, but the move this week is troubling.

Another issue is the costs associated with government support. We have a somewhat nuanced view on the banking sector’s complicity in the financial crisis, what is indisputable is post-crisis regulatory policy impaired profitability and the sector was uninvestable most of this cycle. Certainly, the airline industry is likely to follow a similar path. Today’s government dictate that airlines must refund canceled and rescheduled flights is only the beginning. Expanding the unemployment insurance system to cover independent contractors and therefore, the ‘Gig’ economy, seems likely to broaden public sector efforts like California’s to strengthen labor laws and imperil business models. The broader question of a massive expansion of the debt and deficit is also likely to trigger a political crisis sooner than most market participants expect. Due largely to demographics, entitlement spending will drive begin driving public sector debt higher, the deficit before the crisis was already expanding, so like the early ‘90s and early ‘10s, the federal government will be faced with simultaneous rising debt and deficits. Unlike those two fiscal crises that ended with government shutdowns, rising debt in the ‘20s will be structural, rather than cyclical.

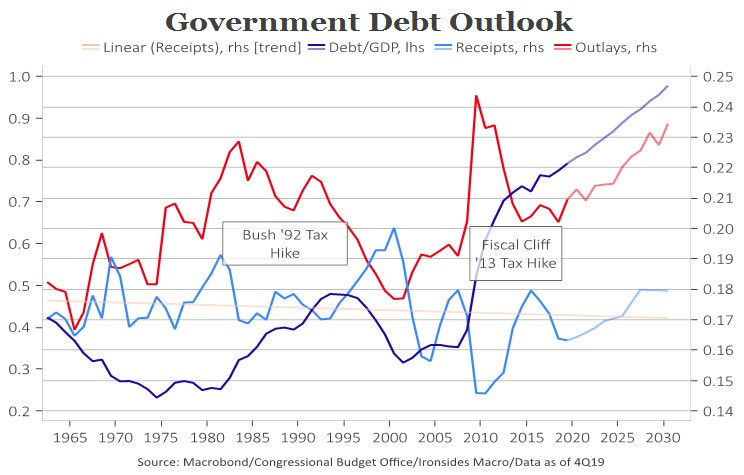

Figure 3: We anxiously await the CBO’s updated analysis of the Federal debt trajectory.

The Econocants are Still Underestimating Dynamism

Several interesting patterns are emerging from the most timely global data, purchasing manager surveys. First, the typically resilient service sectors are absorbing more of the demand shock than the manufacturing sector. Second, although we are skeptical of data from China, March was a recovery month and the rebound was corroborated by surveys from Taiwan and Australia. Finally, and we offer this observation with the caveat that the US has not reached the peak of the pandemic case curve unlike Asia or Europe. The US is holding up better, perhaps due to greater structural flexibility. The upward revision in the Markit March Services PMI from the flash estimate on March 24, to levels far above where China, Asia or European Surveys fell to as they climbed the case curve, offers evidence to support our assertion.

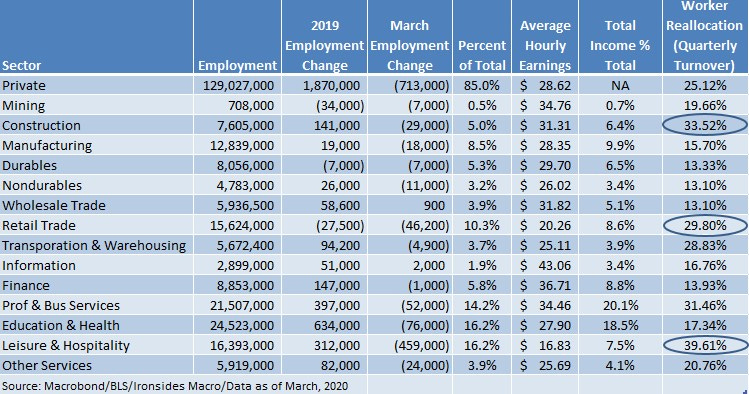

Figure 4: We added the drop in March employment to this chart, notable are declines in the sectors with the greatest turnover. If the population-based controls are removed before excessive damage occurs and the pandemic relief is reasonably effective, these are the sectors best able to deal with turnover.

There wasn’t much encouraging about this week’s labor market data, lowlighted by the 6.648 million weekly initial unemployment claims and the 2.987 million decrease in unemployment from the household survey. What was encouraging was that states were able to process this number of claims and that the SBA small business support program began on Friday and included the largest, most complex banks after Treasury responded immediately to their feedback. Left-leaning economists use crises to promote larger permanent safety nets, however the speed that the legislative and executive branches responded was unparalleled globally. In stark contrast, the totalitarian regime that started the crisis, has increased their reliance on state-owned enterprises, likely further impairing innovation and productivity. We will be watching the rollout of this program closely. Just as important to the effectiveness of the fiscal and monetary policy responses, is the exit strategy to preserve the unique dynamism of the US economy.

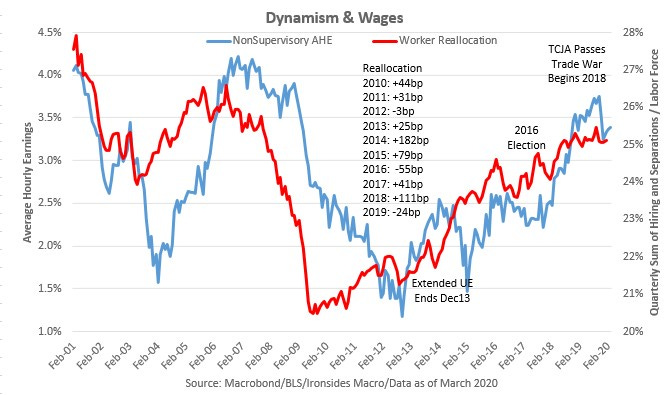

Figure 5: This chart shows how the most generous extensive of unemployment benefits of 99 weeks following the financial crisis likely contributed to a tepid recovery in labor turnover. In 2014, when those benefits ended turnover boomed and labor growth accelerated led by leisure & hospitality, retail and other high turnover sectors. The exit from support is key.

The timing of the phase-out of population-based controls seems less in question, however, the structure and speed is still impaired by a lack of unbiased data. Specifically, we are referring to population samples that determine how widespread antibodies are distributed through the population. There is an interesting study in San Miguel County, Colorado where results should be available early next week. Telluride likely had many visitors in the month of February from what are now hotspots who interacted with locals, it isn’t the petri dish that New York City is, but the testing of the entire population should provide information about how extensive the disease spread through the population. We are hopeful that testing will expand rapidly in coming weeks so that the risks of second waves can be properly assessed as the economic costs of the population-based controls reach their peak.

Figure 6: Earnings forecasts are falling fast led by consumer discretionary, industrials and energy. Earnings season begins in a couple of weeks, it should be interesting.

The Corona Contraction Productivity Shock

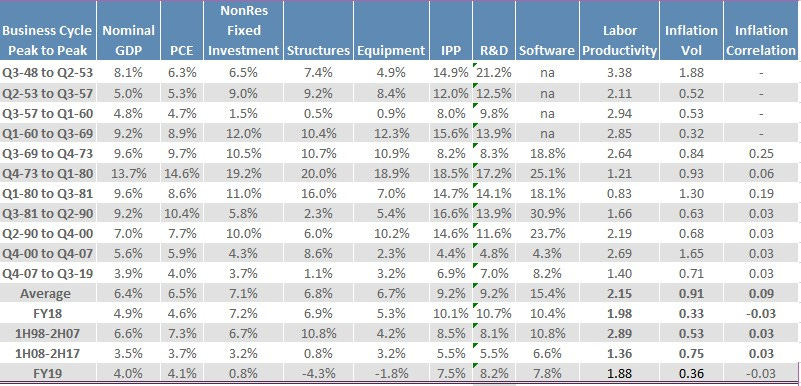

During a call this week, a client asked about the thesis that because the US is a ‘service economy’, the recovery is likely to be longer than in manufacturing economies. The majority of the economic analysis coming out of the street, as is generally the case, is focused on demand side effects, which are undoubtedly going to be unprecedented. Global purchasing manager surveys have seen much deeper declines in the typically resilient services sectors relative to the generally more cyclical manufacturing PMIs. Recessions create a negative productivity shock by reducing investment through weaker business confidence and cash flow and, if the contraction leads to, or is caused by, a financial cycle contraction, a drop in credit supply. Capital investment is one route to stronger productivity growth. Prior to the Corona Crisis, equipment and structures investment were beginning to recover from the Trump Trade War. The more enduring effects come from total factor productivity (TFP) that is believed to result from innovation. We saw evidence the service sector was increasingly adopting technology innovation during the 2018-19 improvement in trend productivity growth and suspect that as the demand shock abates, practices adopted during the crisis will persist and service sector productivity will prove further.

Figure 7: Given the tepid rate of spending on equipment and structures this cycle, it stands to reason that the acceleration in 2018-19 is due to software and R&D.

In the concluding chapter of Alexander Field’s “A Great Leap Forward, 1930’s Depression and US Economic Growth”, Fields attributes the post-war productivity boom to three factors. First, strong manufacturing TFP due to private sector financed research & development. Second, the buildout of the surface road system. The third factor, Field called the adversity/hysteresis effect, is adoption of innovation due to ‘necessity being the mother of invention’. Field went on to describe the effect of the Great Depression on the railroad sector that had been struggling mightily due to the disruption from the auto and trucking sectors. The collapse of credit sent a third of the industry into receivership, however the balance benefited from the adversity/hysteresis effect.

“Beneficial logistical and organization innovations when times were poor persisted when times improved and contributed to permanently higher levels of TFP; as well as the far superior performance of the US rail system in the Second World War compared with the First.”

In the 2020 context of the US service sector dependent economy, S&P 500 R&D was increasing at a 11% annualized rate prior to the virus shock, and after tepid post-global financial crisis 1.36% labor productivity growth, over the last two years productivity accelerated to 1.93%, despite negative manufacturing productivity during the Trump Trade War. The 2020 version of the surface road system is broadband and soon to be implemented 5G. The mother of invention resulting from the 2020 Corona Contraction, could be work from home Friday’s, virtual physician visits, greater parental integration into K-12 education and video happy hours, well maybe not those. Consider work from home Fridays, the new casual Friday, in terms of the effect on emissions and productivity by avoiding commuting time, with management better able to track output after ~six weeks of necessity.

In 2016, Gallup’s Chief Economist published a lengthy report titled “No Recovery, An Analysis of Long-Term US Productivity Decline”, where they concluded that housing, healthcare and education services were the culprits for slower productivity growth.² The share of these three sectors spending relative to GDP increased from 25% in 1980 to 36% in 2015 while education prices increased 8.9 times, healthcare 4.8 times and housing 3.5 times while all-items increased 2.5 times, without sufficient evidence that quality improvements were sufficiently large to justify the price increases. They then backed out the contribution to inflation from these sectors, which increased from 52% in 1980 to 75% in 2015. With that, they then calculated that per capita GDP growth of 1.7% would have been between 3.9% and 4.6% “in the absence of deterioration in these three sectors”.

Figure 8: This is from the Gallup report, we disagree with their conclusion but found their work on healthcare, housing and education important.

²https://news.gallup.com/reports/198776/no-recovery-analysis-long-term-productivity-decline.aspx

Consider how all three of these sectors, the Corona Crisis, and the potential adversity/hysteresis effect. Higher education has been, for decades, in a vicious cycle of spiraling costs facilitated by government non-merit based lending, with no recourse for the universities for bad outcomes, leading to growth in administrator employment, with little growth of the content providing professors. The performance of our K-12 system relative to the world has deteriorated dramatically as teachers unions’ blunt efforts to change incentives to increase meritocracy and introduce private sector competition.³ Full disclosure, my father was a professor at a state university and mother taught elementary school before advising student teachers at another university. We are hopeful that the parental involvement in education learned through necessity during the crisis, will persist when times improve. If there is another stimulus package, forget the roads and bridges, we should invest in broadband and making sure every student has access to the internet. Parents and teachers should be held accountable. We also expect that the trend towards the best professors delivering lectures and content virtually will accelerate and shift the balance of power back towards the product producers, away from the marketing department. That will not happen if the government takes the next step and makes a university education free for everyone. Finally, we have the most confidence that the Corona Crisis will accelerate a developing trend towards technology innovation adoption in the healthcare sector.

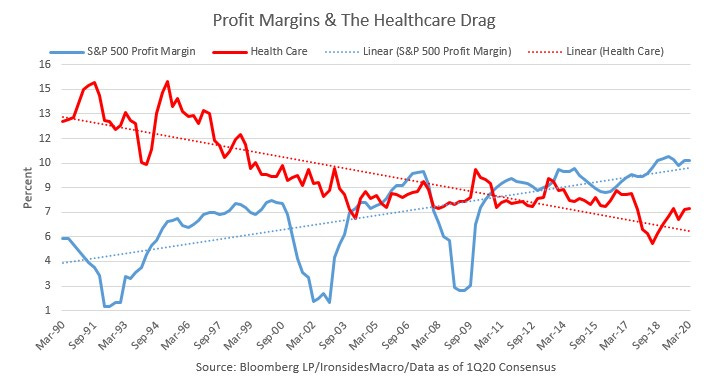

Figure 9: Healthcare margins have been falling for decades, there was evidence they were bottoming. We expect this crisis to accelerate the integration of technology into healthcare delivery.

³Berkeley Schools Leave Every Child Behind

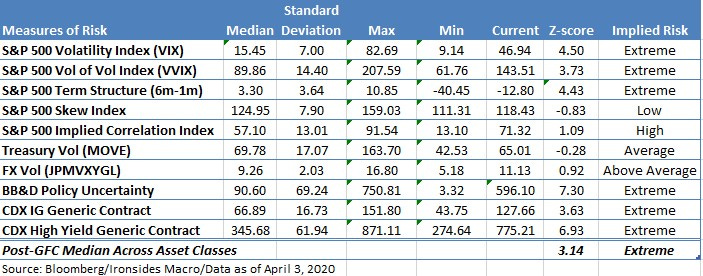

Figure 10: While the VIX, futures curve and vol of vol index remain at extreme levels they dropped sharply during a down week for the S&P 500. This is an unmistakable sign of normalization. Fed actions drove rates volatility back to suppressed levels. Credit spreads widened significantly this week, high yield by 150 bp.

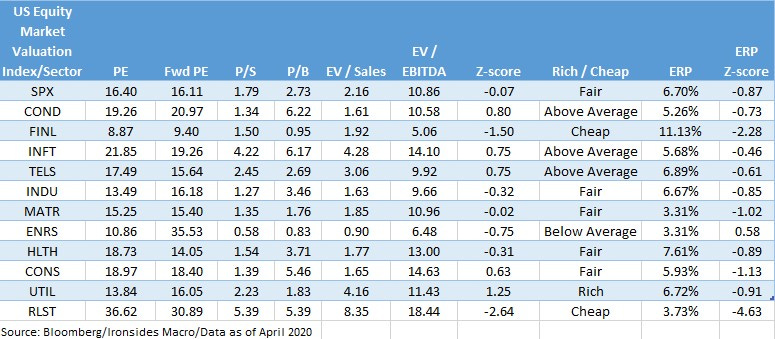

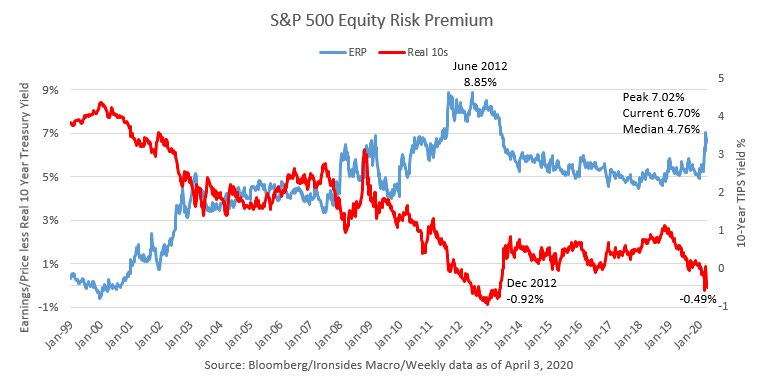

Figures 11 & 12: As earnings estimates decline equities valuation looks less attractive. However, with real interest rates falling further the relative valuation is more attractive.

Barry C. Knapp

Managing Partner

Ironsides Macroeconomics LLC

908-821-7584

https://ironsidesmacro.substack.com

https://www.linkedin.com/in/barry-c-knapp/

@barryknapp

Reading List - Our top recommendation this week has been moved to the top of the list

“A Great Leap Forward, 1930s Depression and US Economic Growth”, Alexander J. Field

“1493, Uncovering the New World Columbus Created”, Charles C. Mann

“Great Society, A New History”, Amity Shlaes

“The Second Machine Age”, Erik Brynjolofsson, Andrew McAfee

“Showdown at Gucci Gulch, Lawmakers, Lobbyists, and the Unlikely Triumph of Tax Reform”, Jeffrey H. Birnbaum and Alan S. Murray

“Grand Pursuit, the Story of Economic Genius”, Sylvia Nasar

“The Rise and Fall of the Great Powers”, Paul Kennedy

“Capitalism in America, A History”, Alan Greenspan & Adrian Woolridge

“Diversity Explosion, How New Racial Demographics are Remaking America”, William H. Frey

“Clashing Over Commerce, A History of US Trade Policy”, Douglas A. Irwin

“Destined for War, Can America and China Escape Thucydides’s Trap”, Graham Allison

“The Constitution of Liberty”, F.A. Hayek

“Judgement in Moscow, Soviet Crimes and Western Complicity”, Vladimir Bukovsky

“1931, Debt, Crisis and the Rise of Hitler”, Tobias Straumann

My next book: “Nudge”, Richard H. Thaler & Cass R. Sunstein

This institutional communication has been prepared by Ironsides Macroeconomics LLC (“Ironsides Macroeconomics”) for your informational purposes only. This material is for illustration and discussion purposes only and are not intended to be, nor should they be construed as financial, legal, tax or investment advice and do not constitute an opinion or recommendation by Ironsides Macroeconomics. You should consult appropriate advisors concerning such matters. This material presents information through the date indicated, is only a guide to the author’s current expectations and is subject to revision by the author, though the author is under no obligation to do so. This material may contain commentary on: broad-based indices; economic, political, or market conditions; particular types of securities; and/or technical analysis concerning the demand and supply for a sector, index or industry based on trading volume and price. The views expressed herein are solely those of the author. This material should not be construed as a recommendation, or advice or an offer or solicitation with respect to the purchase or sale of any investment. The information in this report is not intended to provide a basis on which you could make an investment decision on any particular security or its issuer. This material is for sophisticated investors only. This document is intended for the recipient only and is not for distribution to anyone else or to the general public.

Certain information has been provided by and/or is based on third party sources and, although such information is believed to be reliable, no representation is made is made with respect to the accuracy, completeness or timeliness of such information. This information may be subject to change without notice. Ironsides Macroeconomics undertakes no obligation to maintain or update this material based on subsequent information and events or to provide you with any additional or supplemental information or any update to or correction of the information contained herein. Ironsides Macroeconomics, its officers, employees, affiliates and partners shall not be liable to any person in any way whatsoever for any losses, costs, or claims for your reliance on this material. Nothing herein is, or shall be relied on as, a promise or representation as to future performance. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

Opinions expressed in this material may differ or be contrary to opinions expressed, or actions taken, by Ironsides Macroeconomics or its affiliates, or their respective officers, directors, or employees. In addition, any opinions and assumptions expressed herein are made as of the date of this communication and are subject to change and/or withdrawal without notice. Ironsides Macroeconomics or its affiliates may have positions in financial instruments mentioned, may have acquired such positions at prices no longer available, and may have interests different from or adverse to your interests or inconsistent with the advice herein. Ironsides Macroeconomics or its affiliates may advise issuers of financial instruments mentioned. No liability is accepted by Ironsides Macroeconomics, its officers, employees, affiliates or partners for any losses that may arise from any use of the information contained herein.

Any financial instruments mentioned herein are speculative in nature and may involve risk to principal and interest. Any prices or levels shown are either historical or purely indicative. This material does not take into account the particular investment objectives or financial circumstances, objectives or needs of any specific investor, and are not intended as recommendations of particular securities, investment products, or other financial products or strategies to particular clients. Securities, investment products, other financial products or strategies discussed herein may not be suitable for all investors. The recipient of this report must make its own independent decisions regarding any securities, investment products or other financial products mentioned herein.

The material should not be provided to any person in a jurisdiction where its provision or use would be contrary to local laws, rules or regulations. This material is not to be reproduced or redistributed to any other person or published in whole or in part for any purpose absent the written consent of Ironsides Macroeconomics.

© 2020 Ironsides Macroeconomics LLC.