Talking Tough

Tough forward guidance, curve inversion immersion, fiscally driven consumption, year-end rally update

Seasonality around Thanksgiving is favorable, the World Cup begins Sunday, which will prove a distraction for us, with the holiday and market outlook season looming large. As is our tradition, we will begin with a standard outlook note for the year ahead covering our expectations for the economy, policy and markets in 2023. The following week we will release a note focusing on several secular macro trends we expect to persist for multiple years. We will wrap up our outlook series with our year in review note, in part to help those of you that write similar notes for your clients. Our plan is to publish the first note on December 3rd.

Tough Talk

Thursday morning’s 50-point drop in the S&P 500 and 11bp increase in 2-year Treasuries that pushed 2s10s to -69bp, due to FOMC participant tough talk, culminating with St. Louis Fed President Bullard’s Taylor Rule hypothetical, reminded us of the Friday following the June 2021 FOMC meeting. We got up early that morning to lead off CNBC Squawk Box and delivered a message that, although were quite bearish on the inflation outlook, we did not believe the Committee was ready to start the normalization process. Later in the show Bullard contradicted our message, and 10 minutes after that a bear strolled in front of our office window. As it turns out, Bullard’s hawkish message caused us to get caught offsides due to the 3Q21 inflation soft patch. We don’t believe Bullard misrepresented the Committee’s view. Instead, the combination of the 3Q21 inflation soft patch and the administration’s delay in nominating a Fed Chair caused the FOMC to delay the start of the tightening process.

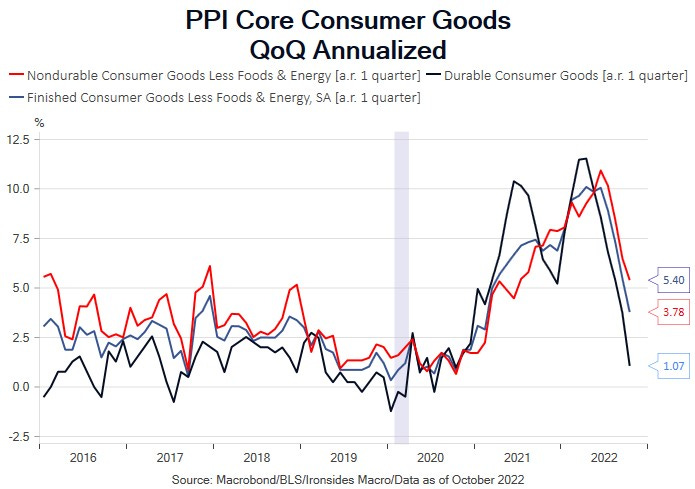

The key to our approach is to make runs behind the defense without getting caught offsides (forget the Gretzky hockey quote, the World Cup begins tomorrow). With that in mind, October single family housing starts fell 6.1% from September and 29% from January. We heard plenty of openings for a Fed pause following a December hike. These openings include Vice Chair for Monetary Policy Brainard’s discussion of wage growth deceleration and global spillover effects, San Fran President Daly’s acknowledgement that shelter costs have peaked and goods prices are cooling rapidly, Waller noting the Zillow House Price Index through October had slowed sharply from the peak in the spring, and Bullard acknowledging weakness in housing and expecting rapid disinflation once the process begins (it has begun, Jim). What we took away from the overabundance of Fed communication this week is that they agreed to slow the pace, that is to say the front-loading process is complete and additional 75bp hikes would require a highly improbable reversal in inflation. The speakers also all appear to buy into the power of their communication strategy. Consequently, in many cases attempts to sound vigilant and focused on the inflation mandate are incongruous with commentary on inflation following cooler October average hourly earnings, the Atlanta Fed wage tracker, CPI, PPI and import prices reports. In other words, they are getting close to a pause but think the markets, and real rate curve in particular, need tough talk, until they don’t.