Silly Seasonals

Silly Seasonals, Inflation is Always & Everywhere a Fiscal and Monetary Phenomenon, Wage Disinflation, Comfortably Long Equities and Taking a Flier on Germany

Silly Seasonals, Sequencing and the Eviler Twin

The financial crisis led to a sharp contraction in economic activity at a time of the year when unseasonally adjusted output surges as companies at full staff following summer vacations push as hard as possible prior to the holidays. Consequently, for the subsequent five years, seasonally adjusted employment growth slowed in the third quarter of the year. Decelerating employment growth led to a series of FOMC unconventional policy responses; QE2 in ‘10, the maturity extension program known as operation twist and mortgage reinvestment in ‘11, and QE3 in ‘12. As soon as those programs were launched employment growth rebounded in the fourth quarter creating the illusion that the transmission mechanism of these programs was more immediate and efficacious than they really were. Our work in our role as Barclays head of equity strategy research showed quite the opposite, the equity risk premium of economically sensitive sectors increased from 5.5% to 7.0% during the non-crisis QE era from September ‘10 through the Taper Tantrum in June ‘13. In short, the Fed’s overreaction to data that was corrupted by an exogenous shock, was counterproductive due to an increase in the cost of capital that impaired capital investment.

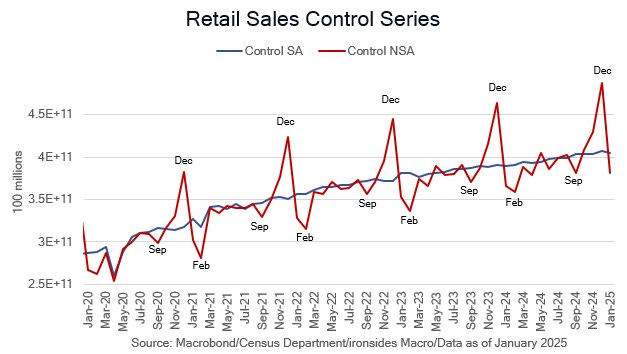

Here we go again; the pandemic policy panic shocked the well-established trend of increased market share of ecommerce retail sales that had reached ~15% in ‘19, up another 5%. The implications continue to ripple through statistical methods to smooth seasonal patterns in employment, wages, prices and sales. Over the last 5 trading sessions, seasonal adjustment factors corrupted the three most important monthly economic reports, the employment situation, consumer price index and retail sales reports. The markets’ reaction to a drop in the unemployment rate, hot wage growth and both consumer and producer prices, and weak retail sales, slightly lower Treasury yields and higher share prices, should be humbling for policymakers. In other words, the collective wisdom of markets looked right through silly seasonals and so are we. There is no change to our forecast for a 100bp reduction of the FOMC policy rate in ‘25, as we’ve explained, 50bp from disinflation and labor slack, and 50bp from a whole of government approach to policy rebalancing (increased Treasury issuance duration, QT through all of ‘25 offset by policy rate cuts.

The Don Quixote’s of economic intelligentsia intensified their windmill titling against President Trump’s plans to Restructure the Global Trading System (here is his head of the Council of Economic Advisors views) this week. This week’s announcement was both inevitable and calculated given the inclusion of non-tariff barriers, as well as the implementation timeline that offers an off ramp for trading partners and sequencing of tax and trade policy. We’ve been emphatic that the much larger risk to investors from our evil twin deficits, budget and trade, is the self-inflicted wound, the federal budget deficit and more specifically, government spending 4% above the 50-year median rate as a percentage of GDP.

In this week’s note we will work through the intermediate and longer-term inflation outlook and implications for investors following the release of CPI, PPI and Import Prices as well as the federal budget update from the CBO and Treasury Department and inflationary implications. Our second section covers the Fed’s employment mandate following the January Atlanta Fed Wage Tracker that validated our view that wage disinflation is likely to persist. The bottom line for investors is our view that a better mix of growth, stronger capital investment, reduced government spending and housing led disinflation, is supportive of our core asset allocation positions of modestly short duration, and overweight economically sensitive cyclical sectors.