Shouldn't Call it a Skip

Deepening inversion, who is buying the bills so far, inflation causation, dynamism overcomes misguided policy

Dangerous Forecasts

This week’s May CPI, PPI, and import prices inflation reports, along with a second weekly initial claims report 10% above the March-May level (262,000), and a slowdown in the 3-month annualized May retail sales control series (ex-autos, gas and building materials) pace deflated with CPI core goods less autos to 0.67% from 3.87% for 1Q23, taken together suggest that the June FOMC hawkish ‘shouldn’t call it a skip’ will evolve into the end of the rate hike cycle. When the Fed meets in July all items CPI is likely to be 3.2%, the weakness in labor income evident in the May employment report will finally catch up to headline nonfarm payrolls, and there will be a preponderance of evidence that Q2 consumer spending slowed to stall speed. With that backdrop we expect the Committee to remain on hold and the most aggressive rate cycle since the early ‘80s will be at an end. However, the Fed’s use of the summary of economic projections as forward guidance intended to tighten financial conditions (increase real rates) and DOT plot dispersion in '25, that indicates there is a significant constituency of Phillips Curve disciples within the FOMC who think a much weaker labor market is the only path to 2% inflation.

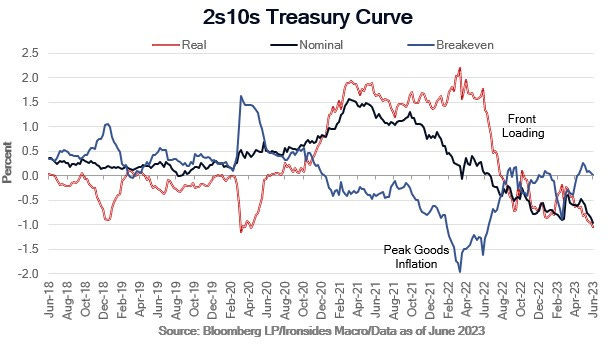

The most concerning reaction to the FOMC meeting was a deepening of the 2s10s nominal Treasury curve inversion. Even with the rally in Treasuries Thursday and selloff Friday morning, the curve inversion deepened. With the 2s10s curve at -96bp, approaching the March low driven by a 104bp inversion of 2s10s real rates (TIPS) curve, underscores the market implied view that monetary policy is more restrictive than any point in decades. While the FOMC passed on an 11th consecutive policy rate hike primarily due to financial stability risks, their forecast, and their portfolio contraction process that is primarily draining liquidity rather than reducing the duration, combined with front-end loaded Treasury issuance continues to be an inexorable curve flattening force. A deeper curve inversion increases the probability of a nonlinear credit contraction that brings on the long-awaited GDP/labor market recession with gross domestic income (GDI) already in recession. The FOMC and Treasury policies are dangerous with banks upside down on securities holdings (1/3 of assets) with little ability to earn their way out of the negative carry on these assets. Following the meeting we expected the hawks out in force in the post-meeting speeches however, the first speech from a FOMC participant, from a credible hawk who likely has Powell's ear, was not hawkish. Waller's speech was notable for what it didn't say. He did not say we need to be vigilant, focus on labor slack, and we need additional hikes, during the speech, though he maintained optionality in the Q&A. Instead, it said the Fed can't always separate macro prudential and monetary policy and a credit contraction is a significant risk. If Waller's view reflects Committee consensus, and we will hear more from the Chair at the semiannual report to Congress next week, the recognition of financial instability resulting from monetary policy, reduces the risk of a severe credit contraction resulting from the Fed single mindedly focusing on inflation while ignoring the risk of a nonlinear credit contraction.

Financial Stability and Macroeconomic Policy, Federal Reserve Governor Waller