Run it Hot

The '17 rally, '18 correction analog, running it hot next year, immigration and the neutral rate, Employment week

Note: Apologies for this week’s delay, we will release an employment preview note this week and return to our regular schedule on Saturday.

The ‘17-’18 Analog

During the first year of President Trump’s first term, despite getting bogged down in healthcare repeal & replace that delayed the passage of the Tax Cuts & Jobs Act (TCJA) until year end, the S&P 500 rallied 20% with very shallow pullbacks. The rally culminated with a 7% steep advance in January due to the 10% boost to earnings from the reduction in the corporate tax rate. While equity investors were focused on earnings and expectations of increased share buybacks and capex, the Fed had begun QT1 in late October. Initially there was little impact on the benchmark discount rate for equity valuation models, the 10-year real rate (TIPS yield). However, in late January amidst the seasonal increase in fixed income supply including the Fed balance sheet runoff, 10-year real rates jumped 30bp. The move in rates accelerated after a sharp increase in average hourly earnings in the January employment situation report in early February. The VIX index began 2018 below 10% but began to move higher alongside 10-year rates, even as stock prices moved higher, before exploding higher in February following the aforementioned employment report. The equity index volatility spike was exacerbated by exchange traded notes that generated income by selling volatility when their share prices crashed, an event referred to as Volmageddon. The year ended with a 4Q 20% drop in the S&P 500 largely attributable to the trade war pushing global manufacturing into recession with the Fed continuing QT and a second year of quarterly 25bp rate hikes.

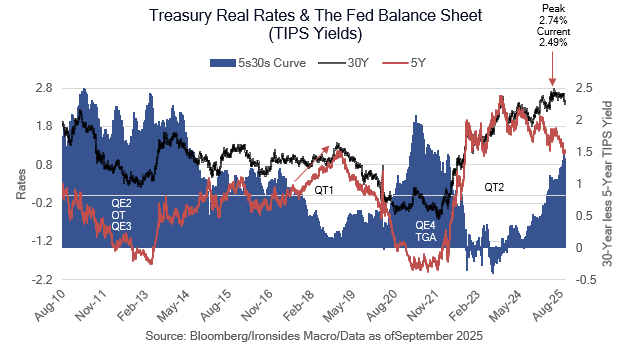

As we like to say, it’s never different this time, but it’s never the same as the last time. During our meetings in NYC last week, one of the topics we discussed with fixed income credit managers was the net supply technical dynamic that was the primary catalyst for the persistent tightening of credit spreads. It seems probable that in ‘26 investment in artificial intelligence infrastructure will evolve from being financed by cash flow from the hyperscalers to an increasing amount of debt. As an example, last week Oracle issued $18 billion in debt. Assuming our forecast for 100bp of Fed rate cuts does spark a recovery in housing net supply of mortgages is likely to increase in ‘26 as well. Additionally, as we discussed at length, when the FOMC ends QT there are two proposals for the System Open Market Account, replicating the maturity profile of current outstanding Treasuries or asset/liability matching. They might choose to do nothing, however either of the restructuring proposals would increase the supply of Treasuries notes in circulation. On balance, although we expect Treasury Secretary Bessent to continue to issue over 30% of total supply in bills, the individual tax provisions (~$350 billion) are likely to increase Treasury supply for a couple of quarters.

It is early for a 2026 outlook, and we expect the equity market to extend the rally into year end with the belly of the Treasury curve rangebound. Conditions in the equity index volatility market don’t appear as extreme, yet historically low implied correlation doesn’t seem sustainable. The monetary conditions are nothing like 2018, however there are a number of paths to greater fixed income supply in 2026 that could lead to echoes of 2018 when equity investor optimism was kneecapped by a real rate shock.

In this week’s delayed note, we will discuss what we learned this week about the economic outlook, cover Fed Governor Miran’s speech on nonmonetary factors (immigration, trade, tax, spending and regulatory policies), and our latest market thoughts.