PTSD or Productivity Boom

Labor & capital investment, the financial crisis that isn't, Fed patience, disinflation and the impressive rally in equities.

We apologize for the late publication, we spent last week in NYC and New Jersey

Misleading Claims

Thursday morning’s surprising drop in initial jobless claims back to the 230,000-240,000 range fooled the algorithmic trading models, not to mention a number of us who watch the data closely. Turns out the seasonal adjustment factors failed to capture the new holiday, Juneteenth, and according to one client, had the BLS used the Memorial Day holiday week seasonal adjustment, claims would have been 275,000. Next week’s note will be a deep dive into the state of the labor market following May JOLTS and June payroll. Given the increase in initial claims to a new range above 260,000 in June and the regional Federal Reserve manufacturing and services surveys that showed employment and hours worked contracting, June could finally be the month where the nonfarm payroll headline reflects softer labor demand evident in hours worked, wages and total labor income. While we caught our initial mistaken reaction to the drop in claims within minutes, 2 to 5-year Treasury notes never gave back the 16bp spike, even after a cool PCED report. The move in the front-end of the Treasury curve further deepen the curve inversion. As we explain below, we did not view Chairman Powell’s roundtable discussion with the heads of the ECB, BOJ and Bank of England and speech the following day as hawkish, in fact he likely began the process of communicating an extended policy rate hold justified by a wider tolerance band around their inflation target. Nonetheless, three weeks into the post-debt ceiling/budget deal surge in Treasury issuance, the Treasury curve is pushing to the top of the ‘23 range and the 2s10s real rate curve 130bp inversion was only deeper during a brief period in November 2008, thereby intensifying the pressure on bank securities holdings. While the liquidity draining process is proceeding as we expected; the persistence and broadening of the equity market rally is approaching the point where we need to check our biases and reconsider our outlook.

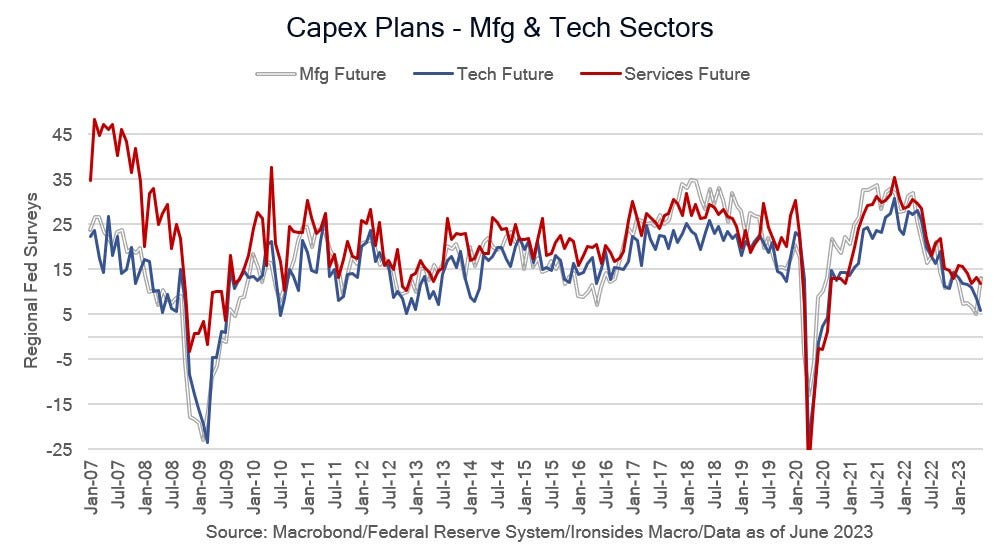

We received a considerable amount of capital investment related data last week. The second revision to 1Q23 GDP showed an even larger divergence between structures (+15.8% quarterly annualized from +11.0%) and equipment investment (-8.9% vs -7.0%) as well as a weaker than trend rate of intellectual property products (IPP) investment at +3.1% revised from +5.2%. Within IPP, R&D was particularly soft at +1.8%, this is likely due to the change from 1 to 5-year tax depreciation allowance. Strong manufacturing physical plant investment, contracting equipment investment and weaker technology investment was also evident in the June Regional Federal Reserve manufacturing and services surveys implying these trends persisted in 2Q. The investment composition looks like modern supply side economics, rebranded this week as ‘Bidenomics’. The Administration’s policies are broadly, government directed investment in partially paid for by eliminating broad tax expenditures on equipment and R&D that allowed the market to allocate capital.

The contraction in real GDI was less deep than the first guesstimate at -1.8% from -2.3%, nominal was little changed at 2.2% from 2.3%, the net operating surplus of private enterprises contracted 7.9% from the first estimate of -9.4% and the drop in corporate profits was -4.1% rather than -5.1%. In short, the profits recession was not revised away, given that the BEA’s measures are consistent with the shallow S&P 500 earnings recession typical of a contraction in real, but not nominal growth, if there is a convergence between GDI and GDP in later benchmark revisions, it’s likely to be at the expense of GDP. At this point, last year’s 27% correction appears to be a recession-related drop, even if it was an earnings recession, rather than a NBER ‘official’ recession. 3Q23 earnings season will provide clues about whether the GDI recession is ending.