Productivity & Policy: Jackson Hole Review

Productivity & Policy: Jackson Hole Review

Economic dynamism, misguided policy, Chairman Powell's speech, Jackson Hole presentation review.

This week’s note was delayed allowing us to read and review the four primary presentation papers at the Kansas City Fed’s annual economic symposium held in Jackson Hole, Wyoming.

Productivity & Policy

Last week’s two market moving events — earnings from the leading artificial intelligence semiconductor company Nvidia, and the Kansas City Fed’s annual economic symposium in Jackson Hole — highlighted a theme we have been writing about all year, namely, the struggle between the dynamic private sector and misguided public policy. Even the monetary policy intelligentsia implicitly acknowledged the costs of policy in terms of productivity and output in the four papers presented at the conference, which we review later in this note. Chairman Powell’s speech was as we expected; he retained optionality for additional policy tightening, but acknowledged the robust disinflationary progress across his inflation framework of core goods, housing services, non-housing services, and crucially, the wage component of services. Chairman Powell dismissed calls for a higher inflation target and the Bullard/Waller thesis that policy lags have shortened, while avoiding the debate about whether there has been a structural change to the equilibrium real policy rate (r*). He began his concluding remarks with the notable quote, “we are navigating by the stars under cloudy skies”, a reference to his first Jackson Hole speech that implied the Fed should be humble about model-based estimates of the neutral policy and full employment rates.

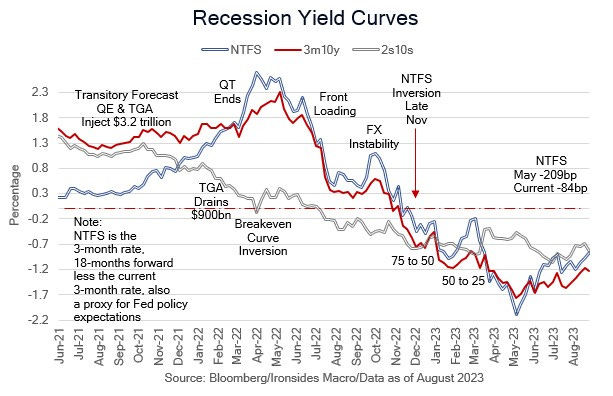

Another important, albeit subtle, shift in tone was the Chairman’s characterization of financial conditions and the credit channel. Rather than describing tighter credit as an intended consequence of policy, without their boilerplate language about the banking system being strong and resilient, the Chairman said the following: “Beyond changes in interest rates, bank lending standards have tightened, and loan growth has slowed sharply.” This sentence was footnoted with elaboration on tighter nonbank credit, a topic also discussed at length in the first paper. Perhaps the Chairman is moving towards our unstable equilibrium view, in short that the deeply inverted yield curve is impairing the flow of credit to the small business sector and is increasingly looking like a systemic risk to aggregate growth.

The market reaction to the speech was mixed. The Treasury curve inversion deepened modestly (2s +6bp, 10s unchanged) — implying a hawkish interpretation — but the equity market appeared to view the speech as dovish and rallied, led by technology and related sectors. For our part, there was nothing in the Chairman’s speech to reduce our confidence that the rate hike cycle is complete, and the low equilibrium real policy rate faction led by NY Fed President Williams is increasingly influential, thereby increasing the probability the FOMC will begin reducing the policy rate in 1H24.