Payrolls & Powell

Fed mandate emphasis shift confirmed, labor demand weakening, bad is good

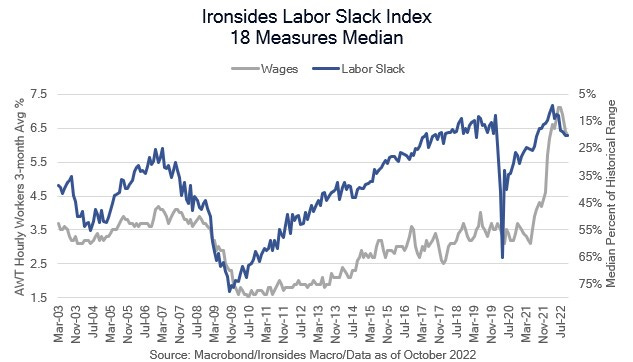

Shrinking Excess Demand

Chairman Powell’s speech was consistent with our view that the mandate emphasis is at an inflection point from singular focus on inflation to a more balanced approach. The market’s agreed, 2-year Treasuries dropped 16bp, 5s30s steepened 12bp, breakevens accounted for 12 of the 19bp drop in 5s and the S&P 500 rallied 122, led by the longer duration, higher valuation, tech and tech related sectors. As we discussed in last week’s note, the markets partied like it was 1995.

Inflation and the Labor Market, Chairman Powell

“To assess what it will take to get inflation down, it is useful to break core inflation into three component categories: core goods inflation, housing services inflation, and inflation in core services other than housing.”

“Finally, we come to core services other than housing. This spending category covers a wide range of services from health care and education to haircuts and hospitality. This is the largest of our three categories, constituting more than half of the core PCE index. Thus, this may be the most important category for understanding the future evolution of core inflation. Because wages make up the largest cost in delivering these services, the labor market holds the key to understanding inflation in this category.”

Between these two quotes Chairman Powell explains that core goods prices are falling as supply chains normalize and though housing services inflation will take time to soften due to the construction of these measures, new lease inflation is decelerating sharply. Consequently, the remaining outstanding issue is non-housing services inflation which is primarily driven by wage growth. As we have explained in recent notes on inflation, non-housing services have been distorted by policy; moratoriums, expanded benefits and measurement issues make forecasting this category fraught with risk. That said, wage growth is easier to measure. Later in the speech the Chairman discusses labor supply but views the constraints as unlikely to change much in the near term. We see reasonably compelling evidence that the demand for labor is softening, in contrast to the Chairman seeing “only tentative signs of moderation of labor demand”. Powell’s comments in the Q&A made it quite clear that risk management drove the decision to slow the pace of hikes and developments in the labor market to determine the terminal rate. In other words, the markets sent an unambiguous signal that the 75bp hikes needed to stop and the Committee is not on autopilot to a 5% terminal policy rate. This brings us to the main subject of this note, Friday’s November employment report.