Payroll Preview & Return of the Policy Put

Policy put, an unemployment rate surprise and the Great Staycation

Partial Pivot to a Policy Put

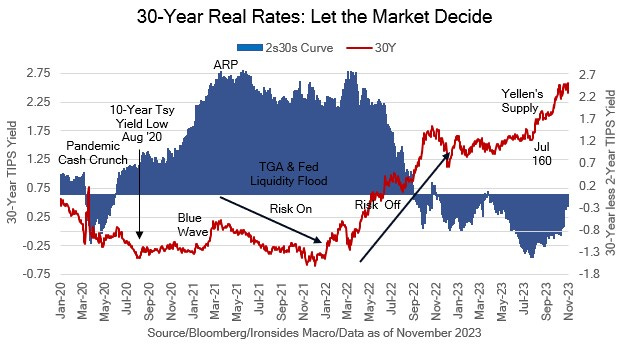

Our first reaction to the rally in Treasuries following the Quarterly Refunding Announcement led by the belly of the curve (2s-7s), despite an increase in issuance in those maturities, was skepticism. To be sure the data cooperated, a second consecutive soft ADP employment report (113,000 in October and 89,000 in September) and an unexpected drop in the October ISM Manufacturing Survey to 46.7 from 49.0, far below expectations of an increase back above the expansion level, were steps towards the Fed’s goal of slower growth. Roughly half of today’s 20bp drop in 5s, 7s and 10s came in the morning, the balance was attributable to something of a confirmation of a concept we introduced following the FOMC’s partial pivot, in a series of speeches prior to the 10-day quiet period before the meeting. As Chair Powell addressed the move in back-end real and nominal rates as well as term premium, he was respectful of the impact of those rates on interest sensitive sectors of the economy, including the banking system, but emphasized persistence as a necessary condition. The way we interpreted their reaction function is confirmation of our overly simplified policy put struck at 5% on 10-year nominal Treasuries. In other words, to avoid a hike at the December meeting, either the labor market and consumption data cooperate (soften), or 10s remain near 5%. We will explore this idea further in Saturday’s note with the benefit of some discussions and perhaps some participant speeches. Our net takeaway is that the probability of a nonlinear tightening of financial conditions is lower, implying 4100 should be the low for the S&P 500 and 10s are unlikely to exceed 5% in the near term. While all the focus is on longer maturities, our necessary condition for a sustainable rally in the Treasury and equity market is a rally in 2s, in other words a bull steepener that stabilizes the banking system and its demand for Treasuries. 4.75% would be a good starting point for yield curve normalization that reduces the damage the bear steepener did to bank balance sheets and profitability.