Overly Restrictive Rate Policy

The Fed's policy mistake, inflation week preview, the risk of a double-dip earnings recession, too early for the growth scare to end

Overly Restrictive Rate Policy

Over the course of 2024 we thought there was a narrow, unsustainable path between a retest of 5% 10-year Treasuries that would lead to a real rate tightening of financial conditions, and the clumsy tightening cycle, passive QT and aggressive rate hikes, that caused the deepest curve inversion since the Volcker Fed, eroding the small business foundation of the labor market to a degree that the economy slowed below potential growth. Pressure on the labor market was evident in 2H23 and 1H24 in virtually all labor market indicators with one important exception, headline establishment survey’s monthly nonfarm payrolls. Last week’s Conference Board Labor Differential, the details of the Job Openings & Labor Turnover Survey, the 2Q Employment Cost Index, and of course, the July Employment report, made it quite clear that the labor market has weakened beyond the point FOMC officials describe as balanced, to unexpected weakness.

Curiously, FOMC officials appear to believe that their credibility as inflation fighters, is applicable to the labor market as well. Although there are fewer post-meeting speeches than usual, virtually every official has characterized the labor market as strong, as if their communication plays a role in business confidence and hiring plans. Even if this were the case for large corporates, the problem is in the small business sector, many of whom have no idea what Federal Reserve officials think. Consequently, either FOMC participants are underestimating negative labor market convexity, or overestimating their ability to stabilize demand. We are long-time skeptics of the role of FOMC communication strategy, credibility and inflation expectations, in the inflation process. Either way, they have already made a policy mistake, and it wasn’t a failure to cut in July, it was their approach to easing, beginning in 1Q22. The issue for the markets is that while a cut in September is likely, participants are not yet prepared to begin the process of rapidly reducing the policy rate to 4%, the level we expect will disinvert the curve, loosen the small bank credit channel, reduce financing costs for small businesses and tighten the spread of mortgages to Treasuries. As the incoming data edges the FOMC towards our forecast for a 50bp cut in September, deteriorating growth expectations are likely to put additional pressure on equities.

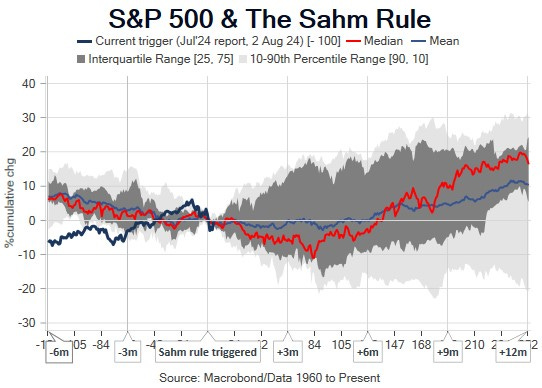

The most important questions we received this week was whether we should frame the growth scare equity market pullback in terms of time or price. A related question was the probability of a recession, which reframed as whether we get a double-dip earnings recession. The difference between a growth scare we suspect is worth 12%-14% off the S&P 500, and an NBER declared recession with a median drop of 24%, is nontrivial. For reasons we will explain in the note, we continue to lean towards the growth scare outcome, however the handful of post-FOMC appearances makes it clear the Committee does not appreciate the labor market negative convexity that is the real lesson of the Sahm Rule. In other words, once the U3 unemployment rate increases 0.5%, it is has always kept rising at least another 1.5%, thereby rendering the FOMC’s Summary of Economic Projections forecast a clear case of ‘it’s different this time’. Our base case for the macro-outlook is weak consumption data beginning next week, and weak labor market data beginning with the first estimate of the annual benchmark revision to the establishment survey just before the Jackson Hole Economic Policy Symposium, continuing with the August data either side of the Labor Day holiday. The catalyst for the equity market pullback was the deterioration in the economic outlook, consequently, with more weak data on the way, it strikes us as too early for the market to bottom.

In this week’s note we will provide a preview of inflation week, discuss the growth scare progression and our thoughts on sector and asset allocation.