November Payroll Preview

We expect a weak report, but will it be enough given the rally in 2s?

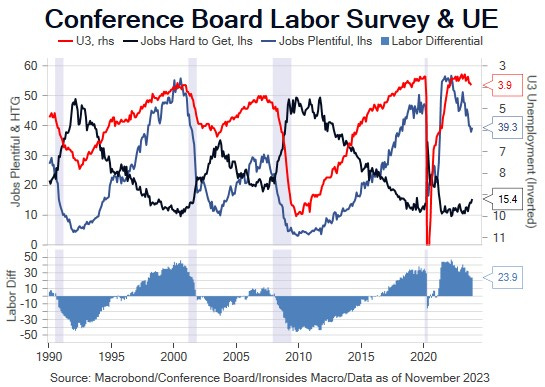

Full Employment Mandate

There are two major economic reports prior to the December FOMC meeting with the potential to close the gap between the September Summary of Economic Projections (SEP) YE24 policy rate forecast of 5.1% and market expectations of 4.04%. First up is Friday’s November employment report, followed by November CPI due on the 12th, the first day of the meeting. We were scratching our head following the September SEP forecast for a modest uptick in the Core PCED to 3.7% in 4Q23, though we thought their YE24 forecast of 2.6% is reasonable. Core PCED cooling to 3.5% in November along with the October CPI report, as well as tertiary and anecdotal data like the Beige Book appears to have convinced the Committee to remove the final 25bp from their forecast. However, the YE24 2.6% forecast still looks reasonable to us, consequently, to close the 1% gap between the FOMC’s YE24 and current market pricing gap further, something in the FOMC’s forecast will have to give and the unemployment rate is the most likely candidate.

While we found their 4Q23 inflation forecast curious, their unemployment rate forecasts of 3.9% for YE23 and 4.1% for YE24, YE25 and 4.0% in the longer run looked overly optimistic in September and even more so today. Consensus for the change in nonfarm payrolls is 187,000 and 160,000 private sector payrolls, an increase from 150,000 and 99,000 in October, boosted by the end of two major strikes. The unemployment rate is expected to remain at 3.9%. Consensus for average hourly earnings is a monthly increase of 0.3% from 0.2% in October that reduces the annualized rate to 4.0% from 4.1%. Given our expectation that underlying productivity growth is 2%, 4% average hourly earnings is consistent with the Fed’s target. Perhaps the last two quarters of robust labor productivity will make the Committee sympathetic to our view, though sustainable wage growth is a reason not to tighten further, not a reason to reduce rates. Additional forecasts are for an unchanged work week at 34.3 and no change to the labor force participation rate of 62.7% following last month’s 0.1% decline in the total and 0.2% drop in the prime age participation and employment rates. We expect another increase in the U3 unemployment and U6 underemployment rates, and see downside risk to earnings, the workweek, payrolls and broader measures of demand including labor income and the aggregate hours index. Even if we get the weak report we expect, the fixed income market is priced for a sharp easing of monetary policy that in our view will not leave the equity market unscathed.