Neutrality

Front loading completion, breadth thrust, inflation falling, but how much, lower housing demand and supply

Over! Did You Say Over?

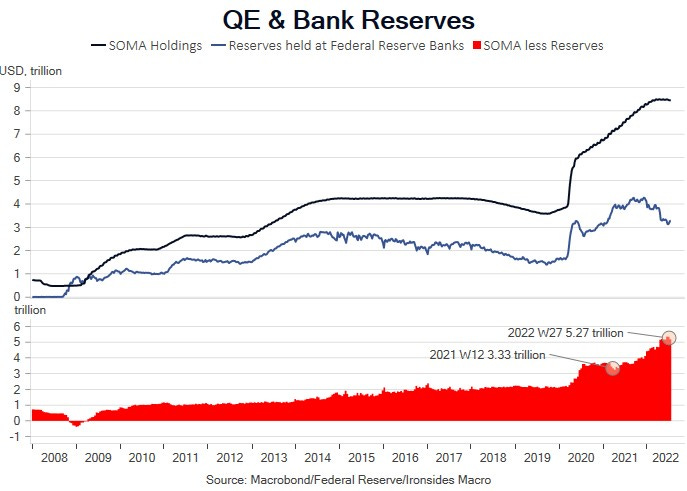

When the FOMC raises the upper end of their policy rate to 2.5% on Wednesday, they will have completed the ‘front-loading’ of rate hikes and will be at their estimate of a neutral rate that is no longer stimulating economic activity. Despite the FOMC’s passive balance sheet normalization process continuing to suppress longer term rates, as evidenced by a negative 45bp 10-year Treasury term premium, an inverted 2-year, 10-year yield curve, and real rates below 1% all the way out to the longest Treasury security of 30 years, the aggressive rate hikes have clearly reduced demand for the largest weight in CPI, housing. While the Fed often claims to have little control over the supply side of the economy, their suboptimal normalization process appears to be reducing the supply of single-family homes, given the second sharpest monthly decline on record in the National Association of Homebuilders Survey and a 19% drop in single-family housing starts from the February peak. Demand for labor also appears to have cooled considerably. A former colleague at Barclays once said the 4-week moving average of jobless claims doesn’t lie, in this case it has risen from an all-time low on April 1 at 170,500 to 240,500. The rate shock has also reverberated through measures of business confidence, putting a strong cyclical and secular capital spending cycle at risk. It might strike some investors as curious that soft housing and manufacturing survey data has been greeted with a strong equity market rally, however, the equity, Treasury and credit markets are sending a consistent message that the front-loading process is complete.

In addition to the likely end of the most acute stage of the 2022 FOMC rate hiking cycle, the European Central Bank ended negative interest rate policy, central bank forward guidance appears to be dead (at least for now), and Tuesday’s ‘breadth thrust’ provided a strong signal that the US equity market’s 1H22 monetary policy normalization correction is complete as well. On the first issue, we would characterize ECB negative rate policy as an abject failure. It did not achieve the objective of raising inflation — the pandemic and Russian invasion accomplished that questionable goal. Further, negative rate policy had several undesirable side effects including impairing credit creation due to weak bank profitability, retarding creative destruction and economic dynamism, facilitating government profligacy, and generating a liquidity trap in Germany that exacerbated their current account surplus. Italian government debt sovereign spreads initially widened (Germany is the benchmark) despite the formal announcement of details of the ECB’s bond crisis tool named TPI (transmission protection instrument), due to the collapse of their 69th post-war government. The ECB also abandoned forward rate guidance, following the FOMC’s 11th hour June FOMC pivot with a late decision to increase rates more than expected and offer no guidance for their next meeting. European bank profitability measures have been roughly half that of US banks since the financial crisis and was integral to our underweight of European equities for the last decade. The end of negative rates is a significant positive step, and we will take a deeper look through earnings season. The larger and more important question for investors is whether Tuesday’s seven standard deviation equity market breadth thrust marked the end of the Fed policy normalization related correction. Technical analysis is not our focus; however, historical analogs are, and the rally off the lows looks very much like a recovery from a Fed policy tightening correction. The pullbacks have much in common with the late stages of the economic cycle, thereby creating investor confusion as to whether the pullback is forecasting a recession. Economically sensitive cyclicals lead the corrections but because these occur when the Fed starts the process, once the policy inflection point is reached like November 1994, the recoveries are broad-based led by cyclicals with defensive sectors lagging badly. One additional note on sentiment, Mike Harnett of Bank America Merrill Lynch’s investor survey contributed to Tuesday’s rally due to extremely bearish investor positioning. We generally prefer what the pay to what they say, and our measures of risk show equity implied volatility and credit spreads are not extended. That notwithstanding, the very low premium for out of the money puts and elevated correlation are consistent with Mike’s survey. Defensive investor positioning was evident for extended periods following the financial crisis, the summer of 2011 following the 20% drop after the end of QE2, is a decent analog. Defensive positioning is a necessary, but not sufficient condition for a rally. Our ‘twin peaks’ outlook, inflation and tightening expectations, is the sufficient condition.

“The advance/decline ratio from Tuesday's rally was 23:1 for the broad market (Russell 3000), which was a 7-sigma event on a rolling one-year basis and the 20th best reading in 15 years. Important market bottoms are sprinkled with these types of thrusts which represent strong demand and help define floors, i.e., support levels.”

John Kolovos, Chief Technical Strategist, Macro Risk Advisors