May Employment

Growth Scare or Rate Shock, The Curves & The Fed, Labor Demand, Wages & Churn

Growth Scare or Resiliency?

Since the Memorial Day holiday, markets have swung from a real rate shock when $183 billion of 2s, 5s and 7s Treasury auctions required decent price discounts that put even more pressure on longer maturity rates, to a growth scare attributable to a negative revision to 1Q24 personal consumption expenditures (PCE), a soft April personal spending report, and another drop in ISM manufacturing. The net effect of softer data on the most widely watched GDP tracking model (Atlanta Fed) was a drop from 4.17% in mid-May, when the model was primarily reflecting late 1Q activity, to 1.85%. The PCE model has driven the decline, the corresponding drop was from 3.94% to 1.75%. The supply concession was the primary catalyst for an increase in 10-year USTs from 4.34% in Mid-May following cooler than expected readings from the big-4 monthly reports, ISM Manufacturing, payrolls, CPI and retail sales, to 4.61%, but with the post-Memorial Day not yet decisively softer data, 10s are back to 4.34%. We walked through this to make the point that the biggest of the big-4, namely payrolls, is likely to determine whether we return to a higher-for-longer/struggling with Treasury supply/0s heading to 5% again environment, or an intensification of the growth scare.

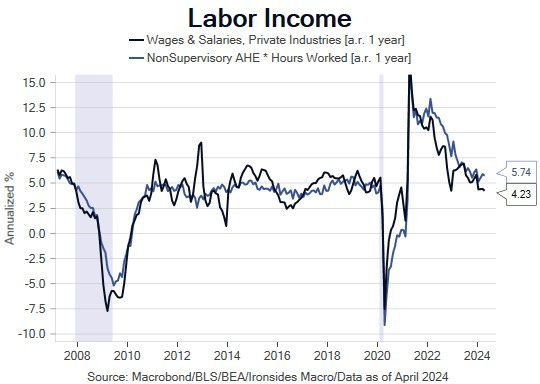

Meanwhile, deep in the Bureau of Labor Statistics weeds, is increasing evidence that demand for labor is weaker than the monthly establishment survey implies. Data from relatively obscure Quarterly Census of Employment and Wages (QCEW) and Business Employment Dynamics (BED) are strengthening the case we and others, including Bloomberg Intelligence’s Anna Wong and Simplify’s Mike Green, have made that the birth/death model is overestimating small business employment. The labor market release most likely to both confirm employment overestimation and catch investors’ attention is the first estimate of the annual benchmark revision just prior to the Kansas City Fed Jackson Hole Economic Symposium, which on its current pace could reduce employment growth for the year ended 1Q24 by 1 million workers. The implications for Friday’s establishment survey are negligible, however, there is reason to expect soft employment from the Household Survey leading to an increase in the U3 unemployment and U6 underemployment rates. In this note we will update the outlook for unemployment and wage growth, and the implications for monetary policy, rates and equities.

We will use Substack chat to relay our initial thoughts Friday morning following this crucial release to paid subscribers and institutional clients.