Liquidity Climate Change

Productivity Boom, Liquidity Climate Change, Tax Expenditures & Economic Efficiency

Is the Light at the End of the Tunnel a Train or a Productivity Boom?

(BN) WILLIAMS: COVID PANDEMIC REDUCED LONG-TERM POTENTIAL OUTPUT

(BN) WILLIAMS: NATURAL REAL INTEREST RATE ABOUT 0.5% IN 1Q

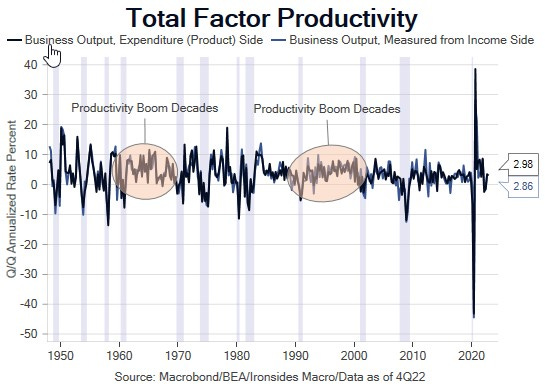

The S&P 500 made a 2023 high this week amidst optimism about what the President calls a budget deal and the Speaker of the House characterizes as a debt ceiling deal, a distinction without a difference. To be sure, a slower growth rate for government spending, particularly unconstrained transfers to individuals, is disinflationary. In the short term, a deal will lead to increased Treasury issuance, which we expect to be funded primarily out of bank deposits. This will increase the risk of a nonlinear tightening of bank credit, but it will also open the possibility of a much earlier than expected end, or at least restructuring, of QT. The debt ceiling, and coming liquidity climate change, is far from the entire story this week. Additional signs housing has bottomed, a handful of hawkish FOMC participant comments, and the coming Treasury supply contributed to a bear flattening of the Treasury curve. The equity market rally took on a life of its own as several notable macro investors, and the Goldman Sachs economics team, went all in on an artificial intelligence driven productivity boom.

We have some sympathy for this perspective, and while we have not seen Goldman’s work on this topic, we wrote in a couple of macro themes year end notes about the coming productivity boom. We expect all three contributors to productivity growth to contribute positively in the ‘20s. Increased labor dynamism will drive faster labor productivity, and whether or not you view work-from-home as immoral, commuting and transportation has been a drag on productivity for decades. Capital deepening from repatriation of manufacturing capacity more reliant on automation and the internet of things rather than cheap labor will increase economic efficiency. Finally, technology innovation adoption will drive faster total factor productivity as the benefits of digitization diffuse to healthcare, the industrial and financial sectors as well as services generally. Faster service sector productivity began late last cycle, AI could accelerate this trend. In other words, we disagree with NY Fed President Williams’ r* natural rate model: the pandemic was a positive productivity shock that increased potential growth, and therefore, the natural rate of interest. That said, we are at the top of the range, and while the rally broadened to include financials and small caps, leaving expensive defensive sectors in its wake, productivity is a slow-moving factor. We view the coming productivity boom as a positive for equities, after we complete the process of adjustment to the excessive pandemic policies. Consequently, there is no change in our view that the next significant move in the S&P 500 is likely to be back towards the December low. We expected the reaction to a debt ceiling deal to be favorable, but like the 2011 episode, the pullback would come after the deal.