Let's Be Independent Together

The collapse in inflation correlation, core growth slows further, the independence bruhaha, another Fed/Treasury Accord to stabilize government debt, bank policy

Note: Next week’s note might be delayed to Sunday evening or Monday morning

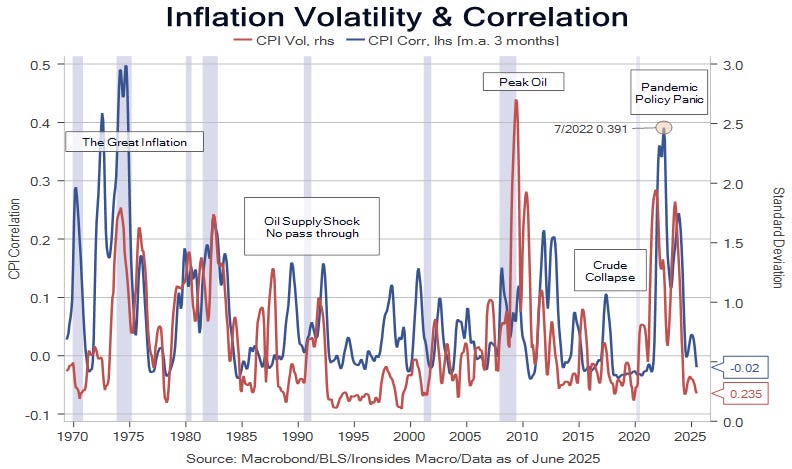

Inflation Correlation Collapse

(BN) WALLER SAYS FED SHOULD CUT RATES BY QUARTER POINT THIS MONTH

Based on June's Summary of Economic Projections, the current target range for the federal funds rate of 4-1/4 to 4-1/2 percent is 125 to 150 basis points above the participants' median estimates of the longer-run federal funds rate of 3 percent. While I sometimes hear the view that policy is only modestly restrictive, this is not my definition of "modestly."

Governor Waller dissented from the curious, in our view, regrettable decision to slow Treasury balance sheet runoff (QT) in March and appears set to dissent on the Committee’s decision to defer resuming rate cuts until September at the July 29-30 meeting. Waller’s arguments, first that tariffs are one-time changes in relative prices, and are a tax, and second that the private sector labor market is showing cracks in the ice, are similar to arguments we’ve been making. This week’s note primarily focusses on the first part of Waller’s case for a July rate cut, before discussing Kevin Warsh’s suggestion that there should be a second Fed/Treasury Accord to stabilize the debt, an idea we’ve been discussing since late ‘24.

In our analysis of inflation, one of the most robust factors suggesting the inflation risk from increased tariffs is minimal utilizes an approach we learned during our decades trading equity derivatives, correlation. In early ‘22, the correlation of the components of CPI reached its third highest reading, only exceeded in the early ‘70s, in mid-’25 it is near record lows. Correlation is a powerful concept, a lesson most investors learned the hard way (losing money), during the Crash of ‘87, the Financial Crisis or any of the many risk-off crises during our 40 years in the markets, cross asset correlation and volatility surged during large, unexpected macro shocks. House prices were long believed to be regional until 2008, asset allocation diversification was supposed to protect investors, but as we know there are crises when these theoretical constructs fail. Those episodes occur far more frequently than the log normal bell curve taught in Statistics 101 implies. Within this context, the pandemic policy panic response, the largest increase in government spending and direct transfer payments to households in US history in early ‘21, monetized by the Federal Reserve buying every bond issued by the Federal government and more than 100% of the supply of mortgages, was a macro shock that caused the third highest correlation of the top 18 components of CPI on record. Macro policy caused a ‘meltup’ in consumer prices.

Today, government spending has slowed sharply, and the policy rate is restrictive for floating rate small business borrowers. Correlation of the components of the consumer price index has collapsed. The contrast between the macro policy in ‘21 when the government sent nearly $400 billion of checks to households with no strings attached, and ‘25 with the government enacting work requirements on transfer programs, could not be starker. The FOMC is looking for risk in all the wrong places, their Achilles Heel is the role of government spending in the inflation process, and they are venturing out onto thinner and thinner ice, except for Waller and Bowman.