Landings & Rebalancing

Slowing labor income, Fed preview, QT, M2, capex, industrial margins and earnings

Slowing, but Still Not Slow

With still only 28% of the constituents of the S&P 500 reporting, a below average earnings beat rate of 2.1% is being met with an average 0.84% daily price increase, underscoring how entrenched the earnings recession narrative is in investor portfolio risk. Even evidence of slowing cloud growth and cautious commentary from the software bellwether failed to derail the rally this week. Incoming economic activity data didn’t explain the equity market rally, January global preliminary purchasing manager surveys were mixed in contraction territory, and while they aren’t deteriorating, they haven’t yet begun the reversal we expect in coming months. The 2.9% increase in the advanced estimate of GDP was flattered by net exports (0.56% contribution) and inventory investment (1.46%), the same sectors that subtracted 3.13% from 1Q and 1.91% from 2Q respectively.

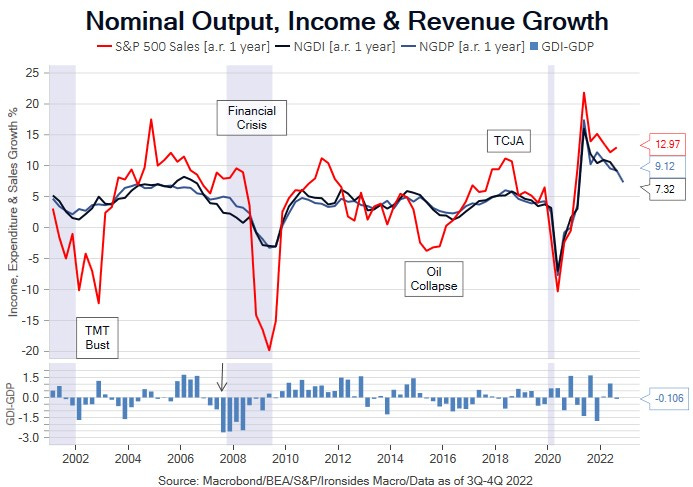

A cleaner way to think about growth in 2022 is full year real output increased 1%, from 5.7% in 2021, while nominal growth slowed to 7.3% from 12.2%. We will not get gross domestic income until the first revision at the end of next month, however, wages and salaries slowed from 8.4% to 5.4% in Q4, while labor income, average hourly earnings times hours worked, slowed from 10.4% to 6.8%. While real and nominal growth slowed sharply, the inflation component fell faster (4.4% in 4Q from 9.1% in 2Q) than did nominal growth (7.7% from 8.5%) in 2H22. Falling inflation, regional Fed manufacturing prices paid and received surveys, as well as strong industrial sector earnings and margins, all increase our confidence in our high conviction view that expectations of margin pressure, integral to the earnings recession forecasts, occurred a year ago. In other words, strategists and investors anticipating an earnings contraction fail to understand the unique characteristics of this business cycle, most likely due to primarily focusing on aggregate demand rather than the supply-side of the economy.

Next week’s macro focus is primarily on the labor market, more so than the FOMC meeting, because the two most influential economists in the Eccles Building steered us to a 25bp hike. On the first day of the FOMC meeting the crucial 4Q employment cost index is likely to confirm the deceleration in wage growth evident in average hourly earnings, Atlanta Fed Wage Tracker, and personal income, thereby strengthening Vice Chair Brainard’s argument that labor demand is weakening. On decision day, the December JOLTS survey will bring into focus Governor Waller’s Beveridge Curve thesis that labor demand still exceeds supply. As we discussed following the December employment report, the focus on openings is misguided given that the two sectors that account for 55% of total openings have rapidly slowing wage growth despite excess demand. Friday’s January employment report is likely to provide more information about whether our call for 25 and done is probable than will the Chairman’s press conference. With the coming end of rate hikes, attention will shift to the Fed’s balance sheet contraction program, the start of ECB QT and the regime change at the BOJ. Thursday night’s hotter than expected January Tokyo CPI triggered another test of the 50bp cap on 10-year JGBs that reverberated across global sovereign bond markets. Interest rate implied volatility has been easing, steepeners (long the front-end, short the back end), put spreads and shorts in the belly of the curve all look attractive around 3.5% for nominal 10s for a move back towards 4% after the Fed pause is confirmed.