June Payrolls: Supply Shock

Lower supply and continued weak demand, but probably not sufficiently soft enough for a July rate cut

Negative Supply Shock

The aggregate takeaway for the FOMC and investors from last week’s (May) labor market data is the Administration’s trade, immigration and spending policies appear to have slowed demand for labor, reduced the supply of labor, and slowed the 2H24 downtrend in wage growth. Fiscal Food Fight, June 7, 2025

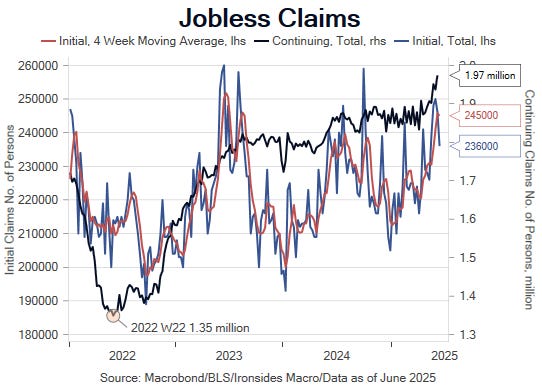

None of the data we’ve received since the May employment situation report has altered our view. The labor differential component of the June Conference Board Consumer Confidence Survey, continuing jobless claims, regional Federal Reserve surveys, ISM manufacturing survey and May JOLTS hiring rate suggest demand was soft in May and probably didn’t improve in June. The more interesting developments are on the supply side of the labor market.

The Bloomberg consensus forecasts are for a 110,000 increase in payrolls, a 4.28% U3 unemployment rate, a 0.28% increase in average hourly earnings and a 62.5% labor force participation rate. In short, slower employment growth, higher unemployment, cooler wage growth and a modest rebound in participation. The data since last month’s report suggests, though not convincingly, you should take the under on payrolls and participation, and over on unemployment and wages.