January Payroll Preview

A sharp drop in job switching driving wage disinflation amidst questions about participation plus some thoughts on the Fed, QRA, QT and the banking system

Falling Demand and Supply Questions

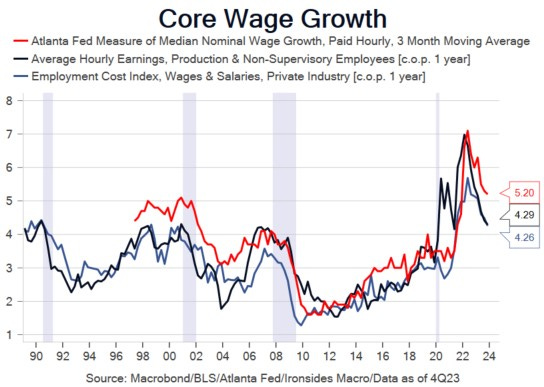

Within our Quadrilemma framework, this week’s pre-payrolls labor market data moved us closer to wage growth below 4%, but further from an unemployment rate above 4%. The data also highlights what we believe is the most important labor market theme, the ‘Great Reallocation’ from mid-’21 through mid-’22 which has evolved into the ‘Great Staycation’. Our work implies at least half of the doubling of pre-pandemic wage growth of nonsupervisory average hourly earnings and the Atlanta Fed Wage Tracker to 7% in 1H22 was attributable to job switching, as opposed to the FOMC’s view that the spike was attributable to diminished labor slack. During 4Q23, our broad slack index recovery stalled, as did average hourly earnings wage series disinflation. However, the more robust employment cost index cooled alongside a sharp drop in job switching. The general FOMC participant narrative is that demand for labor has eased, and the supply is improving, but their characterization of supply is curious given that the sharp increases in 1H23 participation and employment across all age cohorts clearly stalled in 2H23. Friday’s report brings the annual benchmark revision and population control adjustment, consequently, in the words of Bloomberg’s Tom Keene, we and the Fed may need to ‘tear up the script’.