We are placing this note outside the client paywall

Productivity is a Residual

Ironsides Macroeconomics 'It's Never Different This Time' is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

US 2Q PRODUCTIVITY DECREASES 4.6%

US 2Q Unit Labor Costs +10.8%; Consensus +9.5%

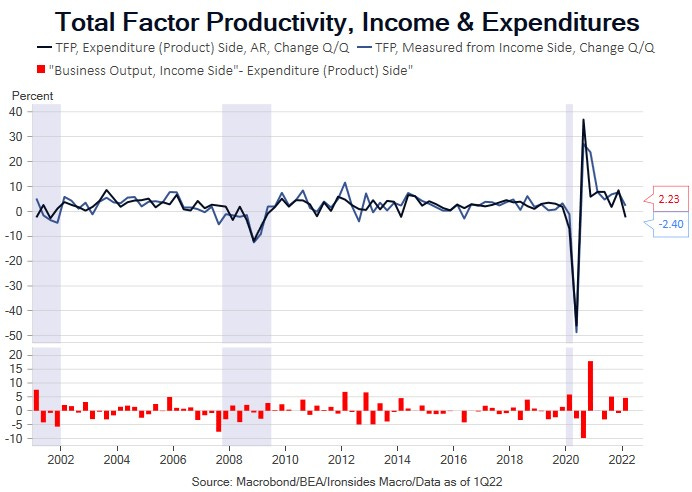

Productivity is a residual variable intended to relate aggregate output to the hours worked. As the economy has evolved from manufacturing to services and intellectual property products, aggregate output has become more difficult to guesstimate. Consequently, the residual variable, productivity, has become increasingly questionable. In 1H22, as consumption shifts from goods to services, the productivity data looks particularly dubious. Our preferred measure of total output, gross domestic income, may be having its day in the sun that leads to a change in focus for policymakers, market participants and government statisticians. Income, not output of ‘stuff’, drives investment in capital, labor and technology, which are the inputs to productivity growth. In 1Q21, real GDI increased 1.8%, nominal increased 10.2% and total factor productivity measured utilizing GDI, increased 2.2%. Using the expenditure method (GDP), productivity fell 2.4% due to the 1.6% decline in GDP primarily attributable to a negative contribution of 3.2% from net exports as supply chains cleared and imports surged. Consider the logic in falling productivity due to a surge in imports as opposed to an increase attributable to surging corporate profits, near record profit margins and 10+% household income growth. Another way to think about this is to compare employment growth from 4Q19 through 1Q22 of -0.7%, to real gross domestic income growth of 6.1%. This looks like surging, not falling, productivity growth to us.

Figure 1: Total factor productivity (TFP) calculated using GDP fell 2.4% in 1Q22 but using gross domestic income it increased 2.2%. We do not yet have the BEA’s first estimate of 2Q22 GDI. We suspect it increased at a similar rate to 1Q.

Turning to 2Q, a decline in GDP of 0.9% was primarily due to negative 2% contribution from inventory investment ($81.6 billion from $188.5 billion) as supply chains cleared. Importantly, inventory investment did not decline, it grew more slowly. In 2020, inventory investment as a percent of GDP fell to its lowest level since the post-WWII ‘49 recession, in late 2021 and 1Q22 it recovered but just as nondurable goods imports surged, consumer demand waned as demand shifted to services. Negative GDP and surging employment led to a jump in unit labor costs and negative productivity measured using the expenditure method. We do not have the BEA’s first GDI estimate, however employee compensation increased 10% in 2Q, down from 11.1% in 1Q. It seems likely the corporate sector net operating surplus was at least as strong as Q1’s 8.4% increase, given a 10% increase in Russell 3000 earnings, the drag on those earnings from companies with large international sales (not counted in gross domestic income), rising sales per employee, and near record profit margins.

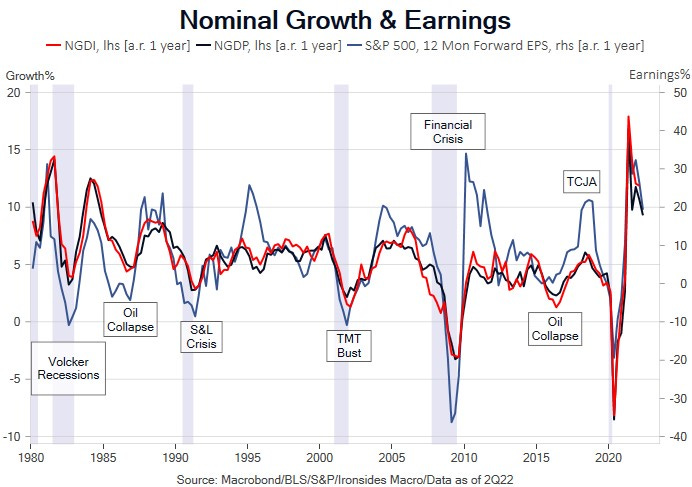

Figure 2: Corporate earnings are an input to GDI, unsurprisingly GDI is a better fit to earnings and sales growth. Income growth drives investment and productivity.

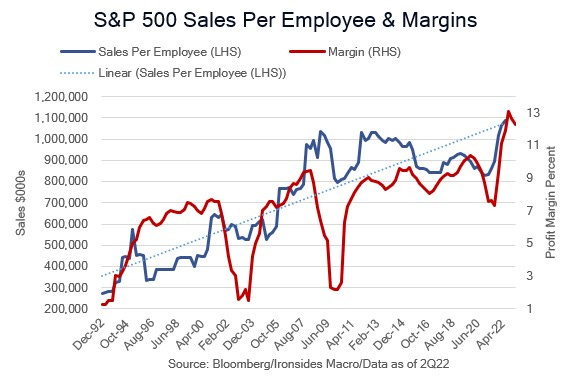

We expect that nominal gross domestic income grew roughly 10% in 2Q, consequently, real GDI was likely positive, implying that total factor productivity calculated using the income method was also positive. In 2Q, S&P 500 adjusted capital investment (Capex plus R&D) increased 15.8% quarter-on-quarter annualized (GDP, GDI math) and 18.5% year-on-year. Sales per employee increased 8.26% quarter-on-quarter annualized. Increasing sales per employee, margins near record levels and strong capital investment growth implies strong productivity growth in the corporate sector and an improving productivity outlook.

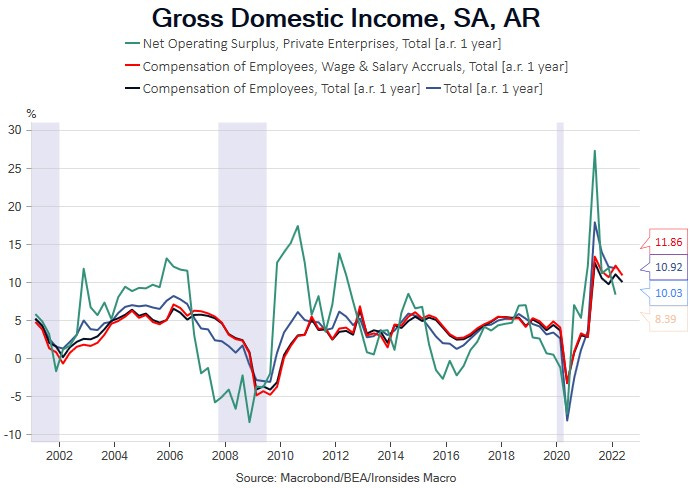

Figure 3: Employee compensation increased 10% in 2Q, down from 11.1% in 1Q. Wages and salaries increased 10.9% vs. 12.2%. Net operating surplus, the broadest measure of corporate income, increased 8.4% in 1Q. Though we don’t have the government’s estimate for 2Q, Russell 3000 2Q earnings growth is tracking 10.3% with 80% of constituents reporting results. Nominal GDI likely remained near 10%, well above the last two cycle’s trend.

In the early days of the pandemic, we reached two important conclusions that differentiated the economic outlook from the financial crisis. First, the pandemic was inflationary, not deflationary. Secondly, productivity in the service sector was surging late in the ‘10s expansion as businesses increasingly substituted capital for labor as we approached full employment primarily through technology innovation adoption. The pandemic accelerated this process. The leisure & hospitality sector is ground zero for this trend: total employment is 1.2 million less than February 2020, however nonsupervisory average hourly earnings are 8.4%, up from 4.5% pre-pandemic and using the S&P restaurant industry index as a proxy, margins are unchanged, and sales are 20% higher. Wages are double the pre-pandemic rate because productivity has surged. The pandemic was a positive productivity shock.

Figure 4: Sales per employees and S&P 500 profit margins imply 10% nominal growth was not accompanied by negative real growth and contracting productivity.

In the ‘20s, we expect a very strong capex cycle, though the ‘Inflation Reduction Act’ and the minimum tax rate on reported profits is a setback for debt financed structures investment that is most sensitive to the tax rate. The pandemic was also the Great Reallocation, it increased fluidity within and across sectors that is likely to boost labor productivity over time and it was a perfect storm for technology innovation adoption. In other words, all three major drivers of productivity, capital, labor and technology innovation, will be contributing to what could be another golden era of productivity growth. Income matters, the Bureau of Economic Analysis should focus on it just as investors do. If you are using GDP as an input to a macro corporate earnings model, you are doing it wrong.

Barry C. Knapp

Managing Partner

Director of Research

Ironsides Macroeconomics LLC

908-821-7584

bcknapp@ironsidesmacro.com

This institutional communication has been prepared by Ironsides Macroeconomics LLC (“Ironsides Macroeconomics”) for your informational purposes only. This material is for illustration and discussion purposes only and are not intended to be, nor should they be construed as financial, legal, tax or investment advice and do not constitute an opinion or recommendation by Ironsides Macroeconomics. You should consult appropriate advisors concerning such matters. This material presents information through the date indicated, is only a guide to the author’s current expectations and is subject to revision by the author, though the author is under no obligation to do so. This material may contain commentary on: broad-based indices; economic, political, or market conditions; particular types of securities; and/or technical analysis concerning the demand and supply for a sector, index or industry based on trading volume and price. The views expressed herein are solely those of the author. This material should not be construed as a recommendation, or advice or an offer or solicitation with respect to the purchase or sale of any investment. The information in this report is not intended to provide a basis on which you could make an investment decision on any particular security or its issuer. This material is for sophisticated investors only. This document is intended for the recipient only and is not for distribution to anyone else or to the general public.

Certain information has been provided by and/or is based on third party sources and, although such information is believed to be reliable, no representation is made is made with respect to the accuracy, completeness or timeliness of such information. This information may be subject to change without notice. Ironsides Macroeconomics undertakes no obligation to maintain or update this material based on subsequent information and events or to provide you with any additional or supplemental information or any update to or correction of the information contained herein. Ironsides Macroeconomics, its officers, employees, affiliates and partners shall not be liable to any person in any way whatsoever for any losses, costs, or claims for your reliance on this material. Nothing herein is, or shall be relied on as, a promise or representation as to future performance. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

Opinions expressed in this material may differ or be contrary to opinions expressed, or actions taken, by Ironsides Macroeconomics or its affiliates, or their respective officers, directors, or employees. In addition, any opinions and assumptions expressed herein are made as of the date of this communication and are subject to change and/or withdrawal without notice. Ironsides Macroeconomics or its affiliates may have positions in financial instruments mentioned, may have acquired such positions at prices no longer available, and may have interests different from or adverse to your interests or inconsistent with the advice herein. Ironsides Macroeconomics or its affiliates may advise issuers of financial instruments mentioned. No liability is accepted by Ironsides Macroeconomics, its officers, employees, affiliates or partners for any losses that may arise from any use of the information contained herein.

Any financial instruments mentioned herein are speculative in nature and may involve risk to principal and interest. Any prices or levels shown are either historical or purely indicative. This material does not take into account the particular investment objectives or financial circumstances, objectives or needs of any specific investor, and are not intended as recommendations of particular securities, investment products, or other financial products or strategies to particular clients. Securities, investment products, other financial products or strategies discussed herein may not be suitable for all investors. The recipient of this report must make its own independent decisions regarding any securities, investment products or other financial products mentioned herein.

The material should not be provided to any person in a jurisdiction where its provision or use would be contrary to local laws, rules or regulations. This material is not to be reproduced or redistributed to any other person or published in whole or in part for any purpose absent the written consent of Ironsides Macroeconomics.

Ironsides Macroeconomics 'It's Never Different This Time' is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.