Intended Consequences

Intended Consequences

Growth is slowing, a credit contraction is looming, the Fed still wants to tighten, earnings trough?

Nothing is Settled

After soft ISM manufacturing and services surveys, soft core capital goods orders, a sharp drop in job openings, a soft ADP employment report, and after the BLS changed seasonal adjustment factors leading to considerably higher initial and continuing claims, we expected a March employment report that sealed the coming FOMC pause. While the report’s details were soft, particularly labor income, FOMC participants don’t seem to be able to look past headline nonfarm payrolls and the unemployment rate. Consequently, we will go into next week’s March CPI report with the market probability of a 25bp hike in May a coin toss.

Another hike would be a mistake. While FOMC participants might believe the market reaction will be muted, the market also expects 2.5 cuts by year end. More significantly, when the near-term forward spread (NTFS), the yield curve the Chairman believes contains the most recession forecasting content, first inverted in late November and was -0.5% at the December meeting, they slowed from 75bp to a 50bp hike. By the January meeting the NTFS was 100bp inverted and the pace slowed to 25bp. Following the dubious January employment, retail sales and inflation data that appears to have been flattered by faulty seasonal adjustment factors, the NTFS disinverted and Chairman Powell triggered iceberg risk by raising the possibility of a 50bp hike. That same curve is -1.38% following growing evidence that the Fed, and market participants got caught by the dubious January data. In the post-financial crisis period, screwy seasonals led to a half a decade of soft 3Q and strong 4Q employment growth, which contributed to the Fed easing in the fall of ‘10, ‘11 and ‘12, just as the data accelerated.

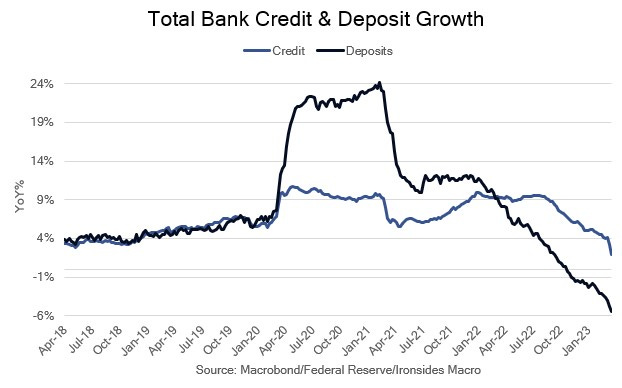

The most significant issue for the FOMC, and for market participants, remains the banking system. At these levels of rates in the belly of the curve the losses on securities holdings are manageable. Silicon Valley Bank’s available for sale portfolio they sold at the lows would be back to the December mark had they been able to hang on. While the losses on assets might be manageable, at the current policy rate, government competition for deposits is likely to lead to a significant contraction in the supply of credit to the private sector. Another rate hike would be reckless.