Inflation is a Fiscal Phenomenon

Twin peaks reviewed, pandemic policy inflation, QT effects: banks and bonds

Twin Peaks Thesis and June Low, Hanging by a Thread

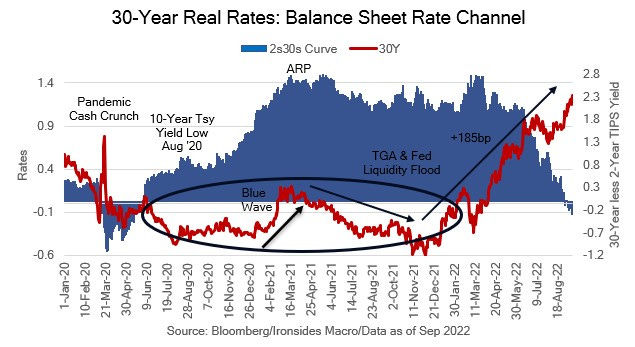

Despite the disappointing August CPI report and resultant increase in market expectations for the terminal policy rate, we do not expect a break of the June 16 3666 S&P 500 low, though the risks of the Fed breaking something, most likely either the housing market or Asian exchange rates (CNH>7), remains acute. As we will explain further, food and core goods CPI are likely to lead a decline in headline CPI to 4% in early 2023, however core services inflation, due largely to pandemic policies that in some cases were made permanent, are likely to create a dilemma for the FOMC in 2H23. Our twin peaks thesis, peak inflation and Fed tightening concerns remains intact, and waiting for the Fed to pivot is likely to be too late for equities given their history of anticipating the end of recessions and Fed tightening market corrections. Market implied inflation peaked in April, consumer inflation surveys peaked in June, and market expectations that the Fed would drive the economy into recession peaked in June following the last-minute decision to tighten by 75bp after guiding to a second consecutive 50bp hike. That said, our forecast for a real rate shock as QT reached its maximum caps, that we expected to cause a taper tantrum aftershock, continues to apply pressure on risk assets. When the Fed was shrinking its balance sheet in 2018, 30bp spikes in 10-year real rates (TIPS yields) triggered a cross asset volatility shock in February (Volmageddon) and the QT Crash in 4Q18. Although the starting point was lower than 2018, 10-year real rates have now increased 100bp from early August. Even on Friday, following the FedEx preannouncement and global recession forecast, real rates are higher across the curve, underscoring the influence of the Fed’s balance sheet that muted their usefulness as an indicator of the economic outlook. The real rate shock is even more impressive given how little the Fed’s mortgage holdings have shrunk given slow prepayments. Financial conditions have tightened considerably since the July FOMC meeting. The terminal policy rate has increased 1.2% (April fed funds futures), the real rate curve has shifted sharply higher to above the 2018 peak, mortgage spreads to swaps are at new highs and the yen, yuan, pound and euro are all under significant pressure. The Fed is only partially responsible for the inflation crisis, as we will explain later, fiscal policy is the larger problem in services inflation. If the FOMC tries to fix the problem in 6 months, they will compound their pandemic policy error. Chairman Powell’s press conference will be crucial to determine if the Fed understands the risks.