Federalies Time

Federalies Time

Expected reaction to the Fed, the pre-Putin Price Hike, Joe Six Pack isn't vulnerable, Fed balance sheet contraction macro and market impact

We have exciting news to share: You can now read Ironsides Macroeconomics 'It's Never Different This Time' in the new Substack app for iPhone.

With the app, you’ll have a dedicated Inbox for our Substack. New posts will never get lost in your email filters or stuck in spam. Longer posts will never get cut-off by your email app. Comments and rich media will all work seamlessly. Overall, it’s a big upgrade to the reading experience.

The Substack app is currently available for iOS. If you don’t have an Apple device, you can join the Android waitlist here.

Channel Check

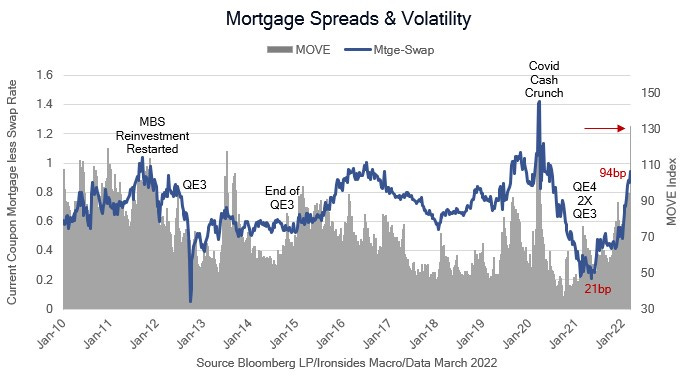

The S&P 500, even after the Russian invasion, is close to the level to which it fell during the January Fed policy normalization correction, and nominal 10-year Treasuries are back to the pre-invasion 2% level. The composition of the 10-year yield has changed; the inflation breakeven component is up 40bp and the real rate component retraced most of the 70bp increase attributable to expectations of tighter Fed policy. The ECB meeting was a bit of a wakeup call, their decision to end their asset purchase program sooner due to their sharply higher inflation forecast was a reminder that developed world monetary policy is incredibly accommodative. We strongly disagree with strategists sounding liquidity alarms, the system is awash with reserves that are so abundant they are impairing bank profitability and — in combination with regulatory policy — impairing the flow of credit to the private sector. Removing counterproductive excessive liquidity will begin the process of ending capital misallocation. In this week’s note we are going to explore the macroeconomic and market effects of the Fed raising their policy rate and beginning balance sheet contraction shortly thereafter. The bottom line is that the economic effect is neutral at worst, and for the banking system a net positive. There has been a significant equity market valuation contraction however, as the Russian risk premium pushed real interest rates back to multi-decade lows despite inflation breakevens at the highest levels since TIPS were introduced in the late ‘90s. The combination means the equity risk premium is exceptionally elevated. There are several channels for large-scale asset purchases to affect markets, policy rate path expectations, the rate of change of real rates, and the volatility channel. The one we were most concerned about, the volatility channel, is now fairly priced for hawkish balance sheet surprises due to the recent spike in the fixed income volatility MOVE index. For this reason, we expect equities to respond favorably to Wednesday’s FOMC meeting.