February Employment Report Preview

February Employment Report Preview

Diminished Recession Risk, Treasuries Vulnerable

This is our first flash update, we will publish these notes periodically when we do not wait to offer our views on macro events until our weekly is released.

Thank you for the interest in our first note, for now these notes are publicly available, please consider becoming a paid subscriber.

The monthly employment for market participants is what Keith Jackson, the legendary college football announcer, called the Rose Bowl: it’s the granddaddy of them all. Therefore, despite our cynicism around the energy Wall Street spends forecasting the net jobs number given how inconsequential it is relative to the size of the work force, and our preference for the job openings and labor turnover survey (JOLTS) as an input into forecasting wage growth, the employment situation report does significantly influence the market implied economic and monetary policy outlook. We generally will not offer a forecast for payrolls and will instead look for evidence of changes in trends in labor market slack and aggregate economic activity. This month’s report could serve to put a nail in the coffin of the 2019 recession thesis and start the process of shifting Fed policy expectations from the next move being a cut, to a hike. Within that context, we are watching the U6 ‘underemployment’ rate, the average hourly earnings data, and signs that the 2018 significant improvement in turnover will continue in 2019.

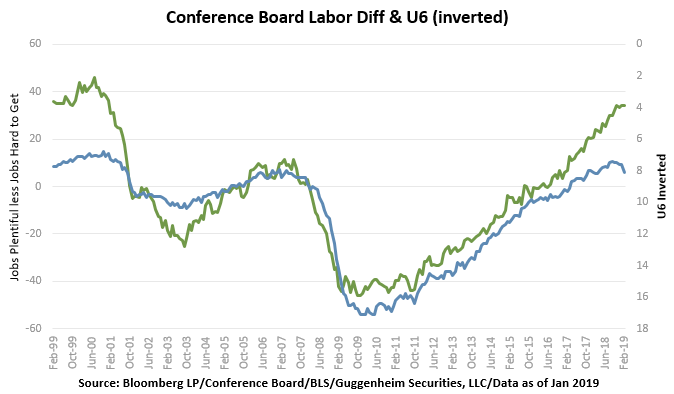

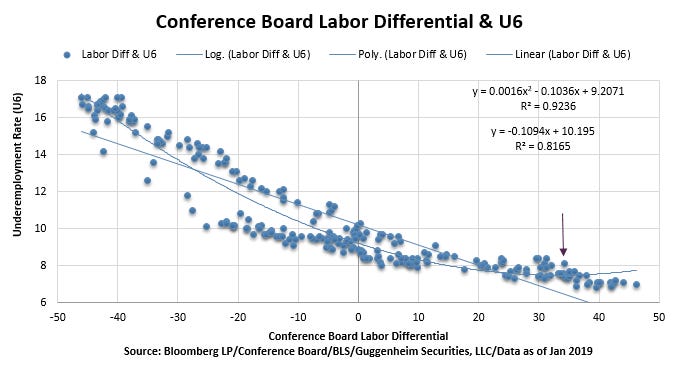

The relationship between the Conference Board’s labor differential indicator, the difference between the jobs plentiful and jobs hard to get questions in their monthly consumer confidence survey, and the U6 underemployment rate is strong though not linear. In recent months, the labor differential has flattened out, but it remains at the peak for the cycle and well above the peak in the ‘00s. While there has been an increase in initial and continuing unemployment claims and the continuing claims rate did increased slightly from an all-time low of 1.1% in October to 1.3%, the stability of the labor differential implies the curious increase in U6 from 7.6% to 8.1% in January is likely to reverse. The U3 ‘official’ unemployment rate also increased in recent months from 3.7% to 4.0% and consensus is for a 3.9% rate in February. On balance, the most widely watched measures of labor market slack should tighten this month.

Our outlook for the wage data is more mixed. The underlying trend is towards stronger wage primarily due to increased labor market dynamism rather than diminished slack; however, while our preferred measure, the Atlanta Fed Wage Tracker, is close to our turnover and slack model forecasts, while the non-supervisory average hourly earnings series (AHE) has overshot our models in recent months. The January total and non-supervisory series, we forecast the non-supervisory series due to much longer history, both increased at a below trend 0.1% month-on-month rate and their year-on-year (y/y) rates dropped to 3.1% & 3.4% from December’s peak of the cycle rates of 3.3% and 3.5%. So, monthly mean reversion argues for a small uptick, however, because the year-on-year growth rates are above our upward trending forecast models, the y/y rates should flatten for a couple of months. To be clear, both our turnover and slack models are forecasting stronger wage growth in 2019.

This morning’s ADP report increased the probability of a strong report as measured by the aggregate hours worked index given the breadth of the job gains by industry, however, the softness in small business employment bears attention given recent weakness in the NFIB Small Business Confidence Survey. The explanation for slower small business hiring may lie in the government shutdown in which case it should prove transitory. The Bureau of Labor Statistics does not capture changes in small business trends well so we do not expect much effect on Friday’s report, but, keep a watch out for next week’s February NFIB Survey. A rebound in business confidence is critical to our positive 2019 outlook.

On balance, assuming the February employment report approximates our expectations, we expect market implied recession to fall further and Fed policy expectations to move marginally towards the discounting the next move being a hike . Specially, cyclical equities should react favorably. The Treasury curve should bear steepen, split equally between inflation expectations (breakevens) and real rates. Finally, our Fed policy proxy (3 month rates, 18 months forward less the 3 month rate) should steepen further from the current level around 0 after beginning the year at -13bp. In other words, we expect a generally strong February employment report to be a catalyst for higher stock prices led by economically sensitive cyclicals, higher longer Treasury yields, a steeper yield curve and marginally tighter credit spreads.

Barry C. Knapp

Managing Partner

Ironsides Macroeconomics LLC

908-821-7584

https://www.linkedin.com/in/barry-c-knapp/

@barryknapp

SEE IMPORTANT DISCLOSURES

This institutional communication has been prepared by Ironsides Macroeconomics LLC (“Ironsides Macroeconomics”) for your informational purposes only. This material is for illustration and discussion purposes only and are not intended to be, nor should they be construed as financial, legal, tax or investment advice and do not constitute an opinion or recommendation by Ironsides Macroeconomics. You should consult appropriate advisors concerning such matters. This material presents information through the date indicated, is only a guide to the author’s current expectations and is subject to revision by the author, though the author is under no obligation to do so. This material may contain commentary on: broad-based indices; economic, political, or market conditions; particular types of securities; and/or technical analysis concerning the demand and supply for a sector, index or industry based on trading volume and price. The views expressed herein are solely those of the author. This material should not be construed as a recommendation, or advice or an offer or solicitation with respect to the purchase or sale of any investment. The information in this report is not intended to provide a basis on which you could make an investment decision on any particular security or its issuer. This material is for sophisticated investors only. This document is intended for the recipient only and is not for distribution to anyone else or to the general public.

Certain information has been provided by and/or is based on third party sources and, although such information is believed to be reliable, no representation is made is made with respect to the accuracy, completeness or timeliness of such information. This information may be subject to change without notice. Ironsides Macroeconomics undertakes no obligation to maintain or update this material based on subsequent information and events or to provide you with any additional or supplemental information or any update to or correction of the information contained herein. Ironsides Macroeconomics, its officers, employees, affiliates and partners shall not be liable to any person in any way whatsoever for any losses, costs, or claims for your reliance on this material. Nothing herein is, or shall be relied on as, a promise or representation as to future performance. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.