Demonetization

The bear steepening continues, pandemic data distortions, QT channels tightening, bank pressure intensifying, not a fat pitch, yet.

Demonetization

“Additional evidence of persistently above-trend growth, or that tightness in the labor market is no longer easing, could put further progress on inflation at risk and could warrant further tightening of monetary policy.” Chair Powell, ECNY October 19

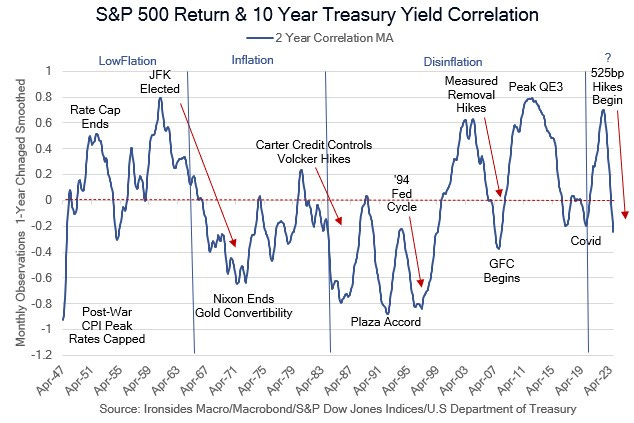

Throughout the ‘10s post-financial crisis quantitative easing regime, we argued that the dominant, and ultimately insidious, effect was not consumer price inflation, it was capital misallocation, or as the Austrian School described it, malinvestment. The first large scale asset program, QE1, facilitated bank balance sheet deleveraging, after the Treasury backstopped the debt of the top nineteen financial institutions. Until March 2009, QE1 had no impact on bank credit spreads; banks selling their highest quality assets would only make their balance sheets more illiquid, at least until they ‘passed’ the stress tests, and the government back stopped their credit allowing them to raise equity capital.

What followed was a series of programs that facilitated socialization of excessive financial and household sector debt. Financial sector debt to GDP ratio peaked at 123% in 4Q08, household sector debt peaked at 98% in 2Q09, by 3Q14, when deleveraging decelerated and consumption returned to pre-crisis trend, those ratios had fallen to 83% and 78% respectively. The final asset purchases of Q3 occurred in mid-October 2014. What began as a market stabilization tool under the Fed’s original lender of last resort mandate, evolved into a tool the FOMC utilized to boost employment and inflation. The same evolution occurred during the pandemic. The ‘dash for cash’ during the peak of lockdown nation — intended to stabilize market functioning of Treasuries and mortgage-backed securities — evolved into support for economic activity without any serious consideration of the second order effects. At the risk of hyperbole, unconventional monetary policy tools, QE, forward guidance and negative rates in Europe and Japan, were the mother’s milk of Modern Monetary Theory. As private sector debt morphed into government debt, the inflationary impulse changed from deflation to inflation. As we wrote in early 2021, while the government might stop sending checks, the mountain of government debt residual would leave a trail of inflation that would persist for the foreseeable future.

(BN) POWELL: FED HAS TO LET RISE IN YIELDS PLAY OUT, WATCH IT

With that background in mind, a Fed partial pivot, skipping the November meeting, a slowing of the every-other meeting rate hike pace, was never likely to be sufficient to stop the insidious bear steepening of the UST curve. We suspected the 5% level for 10-year nominal Treasuries might act as a policy put, however, Chair Powell demonstrated no real appreciation for the damage the plunge in Treasury prices is doing to bank capital, leveraged issuers or small businesses. In other words, he noted the increase in longer maturity yields they are describing as higher term premium, but appeared to view the bear steepening as far less insidious than we do. Equities initially proved resilient to impulsive increases in interest rates in ‘87 and late ‘17/early ‘18 due to sharp recoveries in earnings from recessions led by the energy sector, but ultimately macro instability reverberated from the most important price in the global market system (the benchmark 10-year Treasury) and equities cracked.

Next week we move on from bank earnings to industrials and technology, perhaps turning the focus from the risk of a policy bust to a productivity boom. However, issuance picks up in the belly of the Treasury curve and there will not be much support from bank share repurchases; they are more likely to raise capital than return it to shareholders. In short, after 15 years of debt monetization, the Fed is trying to extricate itself from responsibility for the excessive fiscal debt and deficits, but history argues against debt demonetization. Markets seem increasingly likely to force the FOMC into an unequivocal policy pivot. Until that time, keep some powder dry.

“The unrealized losses in 2022 were significantly higher than during the previous two decades, including during the 2004 cycle, in part due to larger securities holdings. Banks responded to the surge in liquidity from higher deposits in 2020 and 2021 primarily by increasing their investment in longer-term securities rather than loans. Loan growth was tepid in 2020, and interest rates were low through 2021.39 The share of securities with maturities greater than three years was much higher in 2022 than in 2004.”

FDIC Quarterly, October 19, 2023