Convergence

Policy caused divergence of asset prices from fundamentals, employment review and earnings preview

Our 2H22 Outlook: Mostly, They Made it Worse is outside the paywall

Convergence

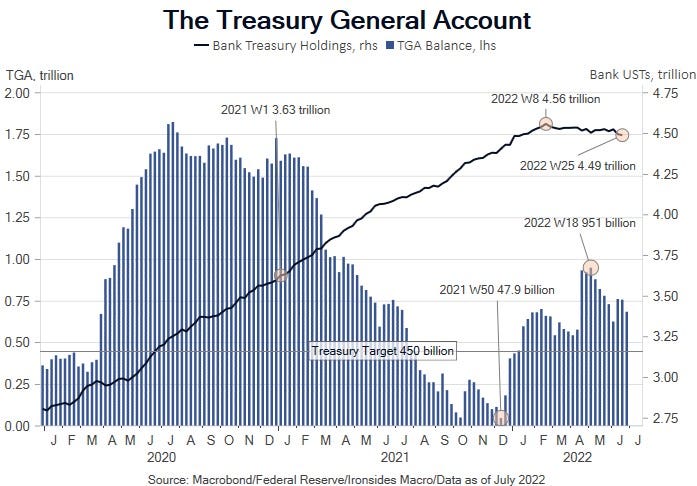

For the better part of a year, markets diverged from underlying economic fundamentals due to the most aggressive post-war fiscal and monetary policy. The Treasury market began 2021 under pressure, not because inflation was accelerating, but rather due to a large increase in supply to absorb the financing of the Democratic Congress and Administration’s $1.9 trillion American Recovery Plan passed using budget reconciliation. The move higher in yields reversed in 2Q21 even as inflation surged, destroying the Fed’s transitory narrative. This was due to the Treasury’s injection of $1.8 trillion into bank deposits and the resultant purchases of Treasuries, as well as the Fed continuing to purchase $80 billion of Treasuries and $40 billion of mortgages per month. The equity market was also diverging from fundamentals in 1H21, particularly, but not exclusively, in the more speculative corners of the market. The manias in SPACs, meme stocks, profitless innovation companies and crypto schemes have been well documented, but for us the premium for upside technology stock calls during the summer of 2021 might have been the most acute sign of excessive liquidity. Pandemic waves, surging inflation, a strong recovery in the labor market and a pivot in Fed guidance (but not asset purchases) had far smaller impact on rates and equity prices than historical valuation analysis implied, due to the massive liquidity injections. For our part we remained fully invested in equities despite stretched valuations primarily due to business cycle analysis until the Fed pivot at the June FOMC meeting. Our business cycle work, as well as extreme valuation, was the basis for our underweight Treasury allocation. The Fed’s passive normalization process, in addition to the Treasury’s aggressive cash management and fiscal stimulus, delayed the inevitable day of reckoning for asset prices until 1H22 when the chaos finally hit the fan. Benchmarking and the bias to assume rational asset pricing is a constant source of investor error, this has been especially pervasive in 2022. If the 20% drop in equities was really signaling a deep decline in earnings, why did real rates (TIPS yields) and the dollar surge and value outperform growth? The answer of course is that the counterproductive fiscal and monetary policy injections in 2021 were hastily reversed in 2022, leading to a painful process of convergence of asset prices and fundamentals. Our work implies that process is now largely complete and the most probable catalyst for the valuation compression to end is evidence that the Fed has passed the maximum point of policy normalization.