CNBC Election Outlook Survey

CNBC Election Outlook Survey

Our responses

We participated in a CNBC Asia survey last week on the expected market reaction to the Presidential election. Here are the survey results and our responses.

We are making this note available to both our free and paid subscribers, to receive updates through the election process on market implied risk please consider becoming a paid subscriber at $89/month or $999/year.

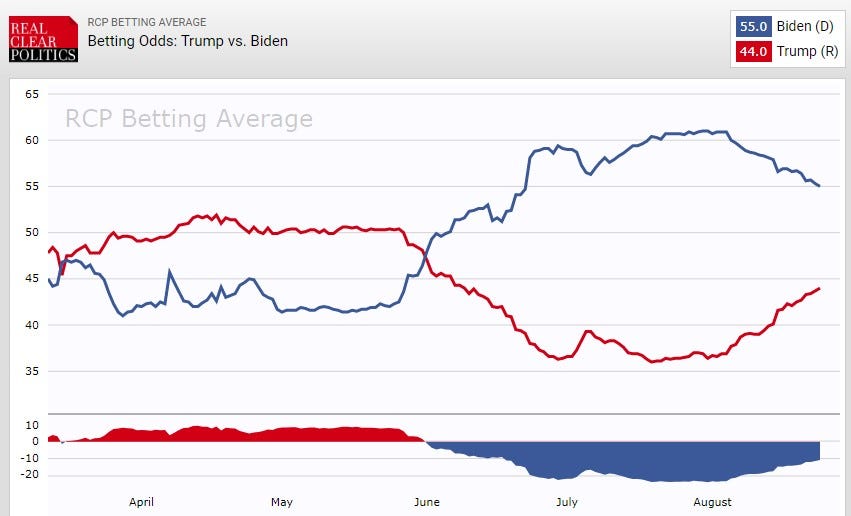

Real Clear Politics Latest Betting Odds

CNBC: 20 strategists predict the U.S. presidential election - and how stocks will react

Here are our responses to the questionnaire from Tanvir Gill, CNBC Asia. Our answers are highlighted.

CNBC Questionnaire – Please answer the following set of questions. Your identity will remain anonymous.

Q1 What do you expect to be the outcome of election 2020?

A) Biden win

B) Trump win

C) Contested election

Additional remarks: The betting markets and polls are tightening and a Biden victory is far from a certainty. More important to the outlook is control of the Senate, if the GOP retains control, the taxation agenda would be difficult to implement. Still, the regulatory environment for banks, healthcare and energy would deteriorate.

Q2 How would the S&P 500 perform 1 month following a declared Biden win?

A) Rally 5%

B) Decline 5%

C) Rally 10%

D) Decline 10%

E) Rangebound between +2% & -2%

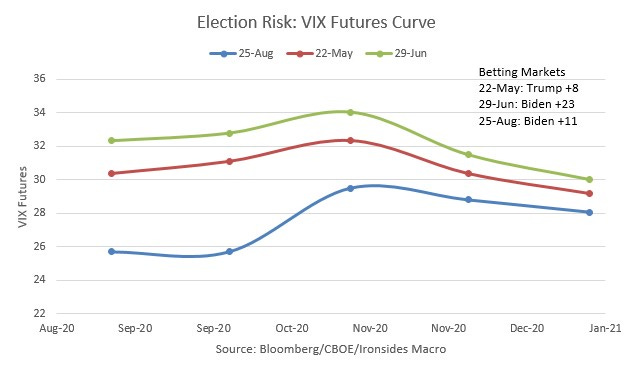

Additional remarks: The term structure of S&P implied volatility is exceptionally steep given that the front month is above 20. Furthermore, skew (premium for out of the money options) is elevated. In other words, despite the S&P making a new high, the index volatility market is discounting a less market friendly outcome. If Biden wins and the D’s take the Senate, the first major move in 2021 will be lower as the taxation agenda takes shape.

Q3 How would the S&P 500 perform 1 month following a declared Trump win?

A) Rally 5%

B) Decline 5%

C) Rally 10%

D) Decline 10%

E) Rangebound between +2% & -2%

Additional remarks: Upside is limited given the lack of a market friendly second term agenda. The primary issue is avoiding the federal government attempting to tax their way out of the pandemic related debt. Trade and immigration policies will be a drag on economic output, regulatory and tax policy are positive; consequently, a Trump re-election is only moderately positive.

Q4 How would the S&P 500 perform 1 month following a contested election?

A) Rally 5%

B) Decline 5%

C) Decline 5% to 10%

C) Rally 10%

D) Decline more than 10%

E) Rangebound between +2% & -2%

Additional remarks: I will no doubt be working on the 2000 analog, though the macro environment is different. The key will be to separate the policy uncertainty from the end of a long cycle in 2020. I haven’t begun this exercise, if the polls tighten further I will though my comments on the index volatility market are applicable to this scenario.

Q5 What would be your December 2020 target for the S&P 500?

A) Above 3600

B) 3400-3600

C) 3200-3400

D) 3000-3200

E) 2800-3000

F) Below 2800

Q6 What would the election outcome mean for US-China relations?

A) Under Trump (Top 3 points) - Much of what is coming out of the Trump Administration at present is political and will fade after the election is over. The trade deal is in both the US and more importantly, China’s interest. Consequently, 2021 will be a good year generally though the tech war will continue and intensify.

B) Under Biden (Top 3 points) - It will be difficult to remove tariffs or engage in other thawing of relations though the rhetoric is likely to be less bellicose. The tech war will continue and intensify.

Barry C. Knapp

Managing Partner

Director of Research

Ironsides Macroeconomics LLC

908-821-7584

https://ironsidesmacro.substack.com

https://www.linkedin.com/in/barry-c-knapp/

@barryknapp

This institutional communication has been prepared by Ironsides Macroeconomics LLC (“Ironsides Macroeconomics”) for your informational purposes only. This material is for illustration and discussion purposes only and are not intended to be, nor should they be construed as financial, legal, tax or investment advice and do not constitute an opinion or recommendation by Ironsides Macroeconomics. You should consult appropriate advisors concerning such matters. This material presents information through the date indicated, is only a guide to the author’s current expectations and is subject to revision by the author, though the author is under no obligation to do so. This material may contain commentary on: broad-based indices; economic, political, or market conditions; particular types of securities; and/or technical analysis concerning the demand and supply for a sector, index or industry based on trading volume and price. The views expressed herein are solely those of the author. This material should not be construed as a recommendation, or advice or an offer or solicitation with respect to the purchase or sale of any investment. The information in this report is not intended to provide a basis on which you could make an investment decision on any particular security or its issuer. This material is for sophisticated investors only. This document is intended for the recipient only and is not for distribution to anyone else or to the general public.

Certain information has been provided by and/or is based on third party sources and, although such information is believed to be reliable, no representation is made is made with respect to the accuracy, completeness or timeliness of such information. This information may be subject to change without notice. Ironsides Macroeconomics undertakes no obligation to maintain or update this material based on subsequent information and events or to provide you with any additional or supplemental information or any update to or correction of the information contained herein. Ironsides Macroeconomics, its officers, employees, affiliates and partners shall not be liable to any person in any way whatsoever for any losses, costs, or claims for your reliance on this material. Nothing herein is, or shall be relied on as, a promise or representation as to future performance. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

Opinions expressed in this material may differ or be contrary to opinions expressed, or actions taken, by Ironsides Macroeconomics or its affiliates, or their respective officers, directors, or employees. In addition, any opinions and assumptions expressed herein are made as of the date of this communication and are subject to change and/or withdrawal without notice. Ironsides Macroeconomics or its affiliates may have positions in financial instruments mentioned, may have acquired such positions at prices no longer available, and may have interests different from or adverse to your interests or inconsistent with the advice herein. Ironsides Macroeconomics or its affiliates may advise issuers of financial instruments mentioned. No liability is accepted by Ironsides Macroeconomics, its officers, employees, affiliates or partners for any losses that may arise from any use of the information contained herein.

Any financial instruments mentioned herein are speculative in nature and may involve risk to principal and interest. Any prices or levels shown are either historical or purely indicative. This material does not take into account the particular investment objectives or financial circumstances, objectives or needs of any specific investor, and are not intended as recommendations of particular securities, investment products, or other financial products or strategies to particular clients. Securities, investment products, other financial products or strategies discussed herein may not be suitable for all investors. The recipient of this report must make its own independent decisions regarding any securities, investment products or other financial products mentioned herein.

The material should not be provided to any person in a jurisdiction where its provision or use would be contrary to local laws, rules or regulations. This material is not to be reproduced or redistributed to any other person or published in whole or in part for any purpose absent the written consent of Ironsides Macroeconomics.

© 2020 Ironsides Macroeconomics LLC.