Big Revisions & Bigger Government

Unmistakable labor market softening, the role for policy in the inflation shock, the recalibration cycle is set to begin with a bang, equal weight breakout

The Revisions & Big Government Getting Bigger

(BN) POWELL: WE DON'T SEEK OR WELCOME FURTHER LABOR MARKET COOLING

(BN) POWELL: COOLING IN LABOR MARKET CONDITIONS IS 'UNMISTAKABLE'

In this week’s note we will discuss the implications of the large negative first estimate of the annual benchmark revision to payrolls as well as some additional employment data released this week. We will also discuss the role of monetary and fiscal policy in the inflation and disinflation processes, and conclude with the implication for markets of the coming FOMC recalibration process we expect to begin with a 50bp cut due to weaker data between now and the September meeting. We begin the note with a discussion of the large negative revision, that was close to our expectations, to private sector employment growth.

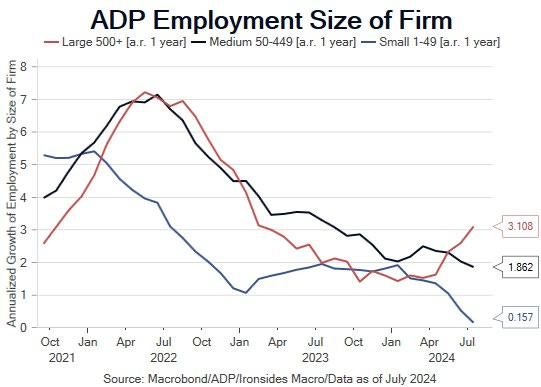

Lost in the rush to dismiss the -818,000 first estimate of the annual benchmark revision as old news was the fact that all of the negative revision was in the private sector, primarily economically sensitive sectors, further widening the gap with government employment growth. One of the curious dismissals we heard was that the low post-pandemic response rate made large revisions inevitable and job growth was still relatively robust in the year ended in March. Our interpretation of low response rates and the large negative revision is that the birth/death model was, and continues to, overestimate small business employment due to a greater number of business deaths. Alongside the first estimate of the benchmark revision, BLS released the Quarterly Census for Employment & Wages (QCEW), about which Anna Wong from Bloomberg Intelligence wrote the following:

“Meanwhile, the 1Q QCEW report shows the four-quarter moving sum in the change of the number of businesses has fallen 51% from where it was a year ago. That suggests the birth-death model’s contribution to payrolls so far in 2024 has been extremely overstated.”

Our Bayesian prior core thesis is that the deeply inverted curve attributable to the FOMC’s aggressive hikes and passive QT placed too much of the burden of demand destruction on small businesses who finance at floating rates from small banks. Here is a passage from the August Dallas Fed Banking Conditions Survey courtesy of The Boock Report:

"Loan volumes were flat in August after increasing in the prior two periods, and loan demand slipped. While overall credit tightening continued, standards and terms stabilized for residential real estate and consumer loans after more than two years of tightening. Loan prices held steady, marking the first time since 2021 that rates didn’t rise. Loan nonperformance continued to increase. Bankers’ outlooks faltered somewhat: They expect a deterioration in loan demand, loan performance and business activity six months from now."

The former head of BLS, William Beach, posted on X (Twitter) the following:

“The big, downward preliminary revisions to non-farm employment (-818,000) announced this morning by BLS probably stem from overestimating the number of firms in the economy. Slowing as well as recovering economies often post challenges for BLS's "birth/death" model, which BLS uses to fine tune their monthly employment estimates. If that's the case, we now have an additional indicator that the economy may be more sluggish than many policy makers believe.”