August Payroll Preview

Powell's Small Business Pain, No August Rebound, B-Curve Recession Threshold, Fluidity Forecasts Cooler Wage Growth, Hours Worked Easing Further

Powell’s Pain

“While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses. These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.”

Monetary Policy and Price Stability, Chair Jerome H. Powell, August 26, 2022

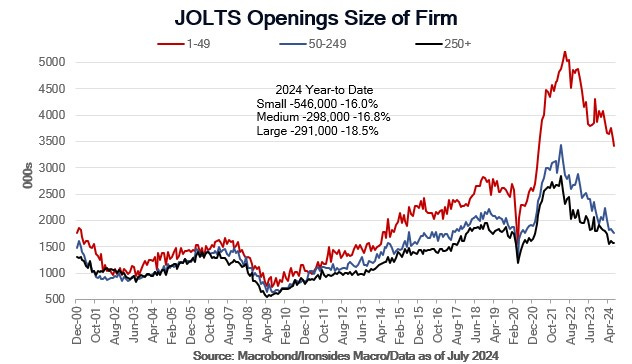

We begin this note repeating a key premise of our bearish labor market outlook we have stated ad nauseum, the FOMC’s passive balance sheet reduction and aggressive rate hikes shifted the burden of Chair Powell’s ‘pain’ to small businesses and households without significant financial and housing assets. Small business employment is more difficult to measure, consequently, it is likely the FOMC, and market participants have been overestimating demand for labor. Following last month’s Job Openings & Labor Turnover Survey (JOLTS), prior to the first estimate of the annual employment benchmark revision, we strongly suggested (forecasted) the Bureau of Labor Statistics (BLS) was overestimating small business openings due to the same issue that led to the negative revision of 818,000 jobs in the year ended March, underestimating the number of business deaths. The first data we looked at after this morning’s release confirmed our suspicions, last month’s year-to-date decline in openings for firms with 1-49 employees was 248,000 (-6.7%), the July report increased the number to 546,000 (-16.0%). The size of the drop in medium businesses (50-249 employees) also increased from 245,000 to 298,000 (-16.8%), while large businesses (250+) openings were relatively unchanged at 301,000 (-18.5%), up from 291,000. The BLS does use the birth/death model to guesstimate small business openings, no doubt the Quarterly Census of Employment and Wages data that led to the -818,000 first estimate of the annual benchmark employment revision was the cause of the reduction in small business job openings as well.

We concluded a month ago that we were already at 1 for one of the Chair Powell, Governer Waller and some other members of the FOMC’s new favorite metric, the vacancies (openings) to unemployment ratio. Sure enough, with the July JOLTS report, it appears we have reached the Beveridge Curve Threshold, and any further weakening of demand will lead to a ‘non-linear’ (accelerating) increase in unemployment. At the risk of repeating ourselves (from Monty Python’s Redundant School of Redundancy), the lesson of the Sahm Rule is the first 0.5% increase in the unemployment rate has always been followed by at least another 1.5%.

The bottom line is we do not expect a bounce back report on Friday, the weakness evident in softer employment growth and increased unemployment was not an aberration. Read on for additional details.