A Liquidity, not a Credit, Cycle

A Liquidity, not a Credit, Cycle

Liquidity reversal, credit cycles, inflation peak, buying opportunity, add some tech

Liquidity Boom/Bust

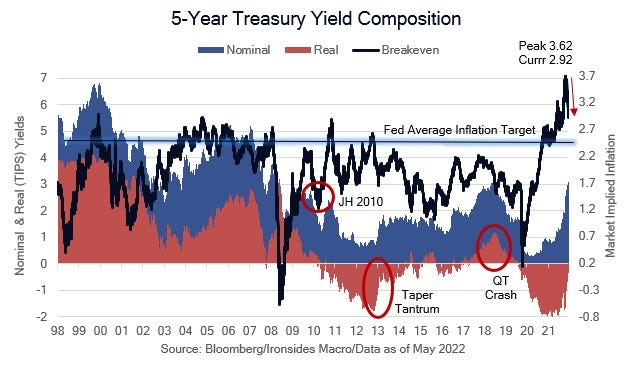

In our 2022 outlook note, Inflation Policy & Politics, the core theme for 1H22 was a divergence between financial markets and the real economy as the 1H21 liquidity torrent turned into a trickle. While this was our forecast, the magnitude of the decline in equities has exceeded our expectations and is down as much as the two largest Fed policy related corrections: in 2011 when QE2 ended, and the 2018 Global QT Crash. The fixed income market response to this week’s inflation numbers that were consistent with our view that inflation peaked was rational; breakevens, the terminal policy rate and bond implied volatility all fell. While the equity market reaction appeared less rational, the decline continued to be led by the most inflated sectors. Excessive monetary and fiscal policy easing led to financial asset, housing, consumer price, and wage inflation. Crypto, EV stocks, innovation names, SPACs, meme stocks and ‘megacap’ tech were the largest beneficiaries of policy engineered asset inflation. When asked on a call what fundamental signposts to look for that would stabilize financial markets, we offered the suggestion that incoming economic activity data was likely to remain strong and a preponderance of decent data would help stabilize an equity market that is now quite reasonably valued. We were reminded of the stabilization of house prices and a strong back-to-school selling season in 2011 while the S&P was falling 19% following the end of QE2, and a dinner with CNBC regulars the night of the December 2018 FOMC meeting when only two of us voted in a poll that there would not be a recession in 2019. We can’t name the other due to Chatham House rules, but rest assured he is not a man predisposed to irrational exuberance and focuses primarily on shorting overvalued stocks.

1Q22 earnings, revenues and margins strongly outperformed expectations led by value/economically sensitive cyclical sectors. Revisions and estimates continue to increase, typically analyst estimates follow share prices, the strength implies robust company guidance. High frequency labor market data remains robust, and spending data shows no deceleration. It defies logic that the partial reversal of the easiest monetary policy setting since WWII, and perhaps most accommodative aggregate policy setting (fiscal and monetary) ever, would cause the economy to immediately tip over. In a 1966 Newsweek article the dean of new-Keynesian economics quipped that the stock market predicted nine of the last five recessions. As it turns out, in the four decades since we began studying economics and finance there has been five recessions and four false alarm 20% or greater corrections; our analysis concludes this one is the fifth.