The majority of the messages we received in response to the FOMC’s 50 bp emergency easing this morning were critical. We have often been critical of Fed policy targeted at lifting a flawed inflation measure towards their 2% target, however, the Fed’s original mission was to be lender of last resort during a financial panic. As we detailed in our latest note “GI Joe with the Kung Fu Grip”¹, we are in the midst of a financial panic. All of the post-crisis analysis concludes that when the Fed’s policy rate gets close to the effective lower bound (zero rates), policy action has to be more aggressive. Chairman Powell’s explanation for the rate cut was that their policy is intended to prevent a tightening of financial conditions and boost household and business confidence. He also mentioned their supervisory role. This is a likely next step, like the early ‘90s during the S&L Crisis, the Fed and other bank supervisors are likely to guide member banks towards regulatory forbearance and easier credit standards.

¹https://ironsidesmacro.substack.com/p/gi-joe-with-the-kung-fu-grip

The reaction to the Fed policy response began with the Friday afternoon’s statement from Chairman Powell. Since that point, the yield curve has steepened aggressively, 5s30s are at the widest level since the Fed began balance sheet contraction in 4Q17. Market implied inflation increased, swap spreads are wider as are cross currency basis swaps, Credit spreads tightened and the high grade market reopened this morning. The dollar index has fallen more than a percent, equities have rallied and our market measures of risk are off their most extreme levels, though they remain elevated. Thus far, their attempts to avoid a tightening of financial conditions are working. For those that are thinking the FOMC could reverse the emergency cuts if the economic impact turns out be transitory, we would remind you a Milton Friedman quote, ‘there is nothing as permanent as a temporary government program’. We are skeptical they will reverse today’s cut prior to the November election.

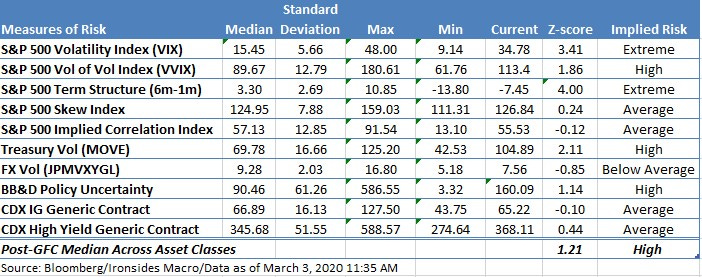

Figure 1: Equity index measures of risk remain elevated, the Treasury volatility index is pointing towards a major refinancing boom and policy uncertainty remains high. Perhaps the most critical of our measures are credit spreads, while they widened sharply they remain in the middle of their post-crisis range.

Prior to last week’s panic we had planned to write about potential Fed rate caps, it won’t be long before we are discussing additional large-scale asset purchases. For now, the Fed had little choice and are unlikely to reduce their $60 billion of Treasury bill purchases per month anytime soon. The Fed acted as the lender of last resort in a financial panic, that is their most important function. It appears to us that critics are conflating post-crisis overly interventionist policy with today’s actions. Criticisms of Friday’s verbal easing and today’s emergency rate cut are misguided. The Fed had no choice, on the margin it is a plus.

Barry C. Knapp

Managing Partner

Ironsides Macroeconomics LLC

908-821-7584

https://ironsidesmacro.substack.com

https://www.linkedin.com/in/barry-c-knapp/

@barryknapp

This institutional communication has been prepared by Ironsides Macroeconomics LLC (“Ironsides Macroeconomics”) for your informational purposes only. This material is for illustration and discussion purposes only and are not intended to be, nor should they be construed as financial, legal, tax or investment advice and do not constitute an opinion or recommendation by Ironsides Macroeconomics. You should consult appropriate advisors concerning such matters. This material presents information through the date indicated, is only a guide to the author’s current expectations and is subject to revision by the author, though the author is under no obligation to do so. This material may contain commentary on: broad-based indices; economic, political, or market conditions; particular types of securities; and/or technical analysis concerning the demand and supply for a sector, index or industry based on trading volume and price. The views expressed herein are solely those of the author. This material should not be construed as a recommendation, or advice or an offer or solicitation with respect to the purchase or sale of any investment. The information in this report is not intended to provide a basis on which you could make an investment decision on any particular security or its issuer. This material is for sophisticated investors only. This document is intended for the recipient only and is not for distribution to anyone else or to the general public.

Certain information has been provided by and/or is based on third party sources and, although such information is believed to be reliable, no representation is made is made with respect to the accuracy, completeness or timeliness of such information. This information may be subject to change without notice. Ironsides Macroeconomics undertakes no obligation to maintain or update this material based on subsequent information and events or to provide you with any additional or supplemental information or any update to or correction of the information contained herein. Ironsides Macroeconomics, its officers, employees, affiliates and partners shall not be liable to any person in any way whatsoever for any losses, costs, or claims for your reliance on this material. Nothing herein is, or shall be relied on as, a promise or representation as to future performance. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

Opinions expressed in this material may differ or be contrary to opinions expressed, or actions taken, by Ironsides Macroeconomics or its affiliates, or their respective officers, directors, or employees. In addition, any opinions and assumptions expressed herein are made as of the date of this communication and are subject to change and/or withdrawal without notice. Ironsides Macroeconomics or its affiliates may have positions in financial instruments mentioned, may have acquired such positions at prices no longer available, and may have interests different from or adverse to your interests or inconsistent with the advice herein. Ironsides Macroeconomics or its affiliates may advise issuers of financial instruments mentioned. No liability is accepted by Ironsides Macroeconomics, its officers, employees, affiliates or partners for any losses that may arise from any use of the information contained herein.

Any financial instruments mentioned herein are speculative in nature and may involve risk to principal and interest. Any prices or levels shown are either historical or purely indicative. This material does not take into account the particular investment objectives or financial circumstances, objectives or needs of any specific investor, and are not intended as recommendations of particular securities, investment products, or other financial products or strategies to particular clients. Securities, investment products, other financial products or strategies discussed herein may not be suitable for all investors. The recipient of this report must make its own independent decisions regarding any securities, investment products or other financial products mentioned herein.

The material should not be provided to any person in a jurisdiction where its provision or use would be contrary to local laws, rules or regulations. This material is not to be reproduced or redistributed to any other person or published in whole or in part for any purpose absent the written consent of Ironsides Macroeconomics.

© 2020 Ironsides Macroeconomics LLC.