Long Policy Lags

Long Policy Lags

Recalibration or Recession, Long and Variable Lags, Policy Efficacy, 3 E's Outlook Remains Negative

Recalibration or Recession? The Race to 4%

(BN) WALLER: COULD CONSIDER 50BP CUT AGAIN IF JOB MARKET WORSENS

(BN) WALLER: INFLATION SOFTENING MUCH FASTER THAN I EXPECTED

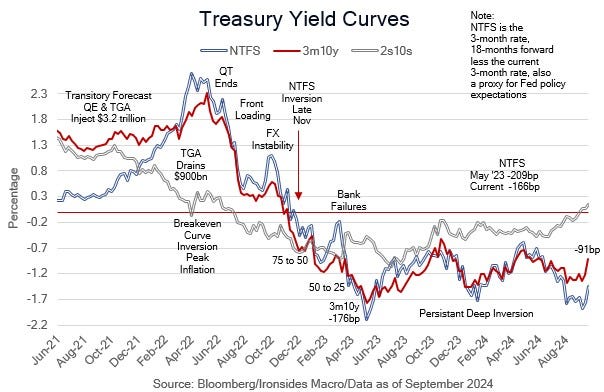

The FOMC’s decision to front load what they hope is a recalibration of policy, rather than an exercise in chasing rising unemployment, was attributable to the risk of a nonlinear increase in unemployment was significantly greater than a reversal of the two-year disinflationary trend. Governor Waller, speaking for himself, told CNBC that the components of CPI and PPI that feed into PCED suggested inflation was too low over the last four months, and convinced him that a larger cut was necessary. We are suspicious that inflation was the catalyst for beginning the process with a 50bp, recent disinflation is overly reliant on global factors causing core goods and energy deflation, while domestically determined shelter and non-housing services inflation are well above the FOMC’s target. A similar pattern developed in 2H23. We have been long expected the Committee to begin aggressively cutting rates once the unemployment rate decisively exceeded 4%.

Regardless of the weights the Committee placed on the inflation and employment mandates, they took an important first step to a sustainable disinversion of the 3m10y banking proxy curve. We expect labor data to continue to be soft and suspect the softness evident in labor and capital investment will spread to consumer spending in the lead up to the holiday season. Consequently, we expect another 50bp cut in November and expect the Fed to cut the bottom of the policy rate band to below 4% at the late January (27-28) meeting (25 in December and January following the first two 50bp cuts). The important question we will discuss in this week’s somewhat abbreviated note, and in the coming weeks, is whether we can avoid weakness in the small business sector and labor market from becoming widespread. In short, can the Fed recalibrate the policy rate to 4%, or will the small business earnings recession spread and the Sahm Rule history repeat.

If you were watching financial television, you likely heard the history of stock market forward returns when the Fed begins the cycle with a 50bp cut is dependent on whether a recession develops. Most of our meetings on our road trip to Boston and NYC covered recession risk. We will discuss the recession risks in this week’s note, but before we delve into the outlook it’s important to recall that we’ve had inventory, housing, manufacturing, corporate earnings and now small business recessions since the beginning of ’22. We had the largest inventory expansion and contraction since the late ‘40’s when supply chains cleared in 2H21, leading to inventory liquidation with trailers full of goods sitting at Target and Walmart parking lots, and a 2% 2Q22 negative GDP contribution from inventory investment. As inventories stabilized, residential investment collapsed and subtracted 1.3% from GDP in 2H22. In 4Q22, corporate earnings began a 9-month contraction that ended in 2Q23. The trough flattered 2Q24 12% earnings growth, 3Q24 estimates are for 5.4% growth, and ex-technology and communication services, the sectors benefitting from the Gen AI investment boom, earnings are expected to be barely positive at 1.6% according to Lipper Analytics. The series of rolling recessions didn’t end there, the regional banking sector marked the beginning of a small business and banking recession that appears to have escaped the attention of policy makers primarily due to poor real-time measurement of small business employment.